"By lowering rates, central banks accelerate growth and by raising rates, they slow it". That's standard practice. But Richard Werner says central banks have it all wrong.

Werner says central bank policy depends on a negative correlation between interest rates and economic growth. It doesn't work that way, he says. "If you plot the nominal GDP growth rate against nominal interest rates, say, a scatter plot, you will find a positive correlation." A positive correlation, he says, not negative. If Werner is right, this is a major conceptual shift.

I watched a Werner

interview two weeks ago, and did some

reading. Every day since, I've been drawing his scatterplot. It fascinates me. I've started writing about it half a dozen times. Until now, my response has died every time. It is a difficult response to write, due to both the "major conceptual shift" and the "if Werner is right".

For starters, Werner's choice of data troubles me. If you

plot the nominal GDP growth rate and nominal interest rates, you see both going high during the Great Inflation

because of the great inflation. You see both going low after the financial crisis

because of the financial crisis.

Nominal GDP grew rapidly during the Great Inflation, because of inflation. At the same time, policy (and creditors) pushed interest rates up to very high levels because of inflation. Inflation caused both growth and interest rates to rise to high levels, and then to fall when inflation receded. Movement in the same direction. That's a positive correlation.

More recently, a different set of special circumstances arose. The financial crisis and the Great Recession drove economic growth to unusually low levels. In response, our central bank dropped interest rates to the floor. Again, unusual circumstances created a positive correlation -- this time, low growth and low rates.

These positive correlations arise from sources other than the relation between economic growth and interest rates. If you mix such times with normal times, in a single picture of the economy, you distort the norm and create a hotbed of doubtful GDP/interest rate correlations. To add an overall trend line to such a mix of data would be absurd.

To be sure, I

don't see Richard Werner showing trend lines on his scatterplots. But I do see him proclaim

the scatter plots on the left-hand side of the graph show a distinct positive correlation.

I do see him proclaim

The positive correlation of both curves is obvious.

And I do see him proclaim

instead of the proclaimed negative correlation, interest rates and economic growth are positively correlated.

Werner doesn't need to

show a trend line. The positive correlation is obvious, he says. He doesn't need to show the trend line to see it. But he does not by his power of vision manage to escape the absurd.

Me? Yeah, I show the trendlines.

Does a positive correlation exist in the "normal" economy? Perhaps. But if we're going to look into it, we should exclude the data since the financial crisis, and we ought to strip inflation out of the numbers we will be looking at. For starters.

Now you know what we're doing today.

I thought I might be confused about what Werner is saying, so I checked: He is not speaking of what people in general think about central bank operations. He refers

explicitly to the views expressed and the actions taken by central bankers:

Recently, central banks have been lowering rates, while proclaiming that this is a measure to stimulate the economy.

He disputes their story:

To the contrary, empirical evidence shows that ... interest rates and economic growth are positively correlated.

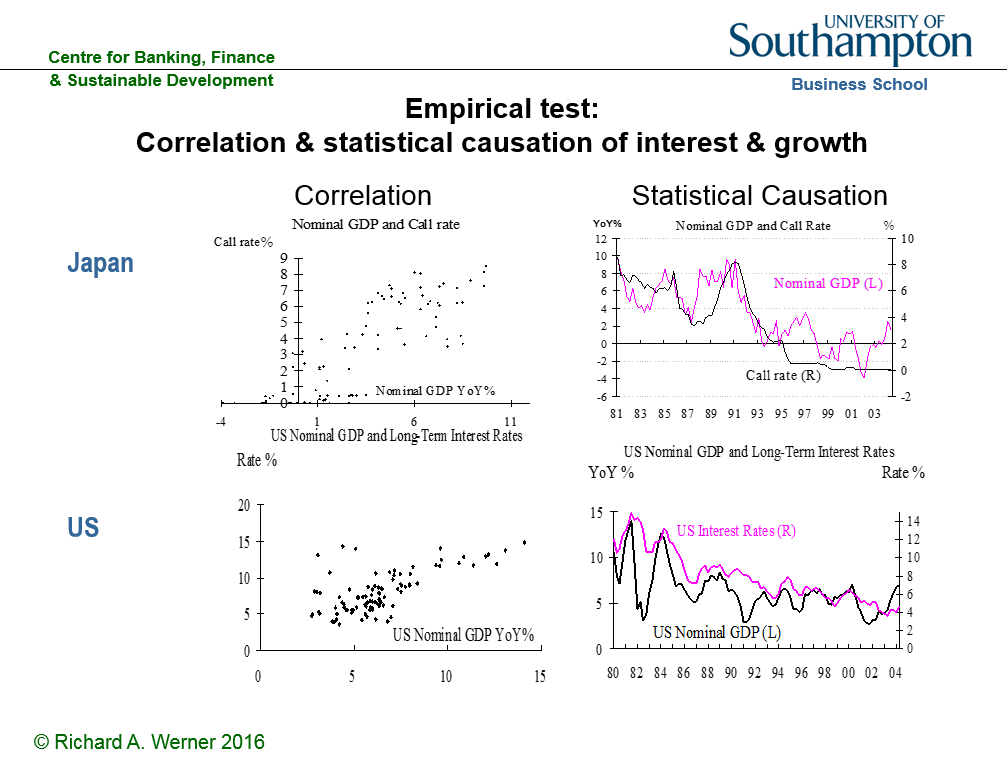

Werner uses a scatterplot to show correlation. Oddly, however, his scatterplot of U.S. data does not use the short-term interest rate that our central bank uses to influence the economy. Werner uses a long-term rate in his scatter. To test the idea that central banks influence growth by changing rates, it seems to me the scatterplot should use the same short-term rate that is used by the Fed.

Granted, the scatterplot might show a positive correlation for any interest rate you pick. But if you're going to challenge the Federal Reserve on interest rate policy, shouldn't you use the same interest rate that the Federal Reserve uses?

For my scatterplot data, then, I will use Real GDP and the inflation-adjusted FedFunds rate. My inflation-adjusted FedFunds calculation is similar to

Bill McBride's from a dozen years back. I'll use the Effective Federal Funds Rate less "percent change from year ago" of the CPI:

|

Graph #1: FEDFUNDS (blue) and Inflation-Adjusted FEDFUNDS (red). Quarterly Data

The area between the red and blue lines, that's all inflation |

These days the Fed prefers PCE to CPI. But I'll be cutting "these days" off the chart. And the Fed only

switched from the CPI to the PCE in 2000. My scatter data goes back to the 1950s. I'm sticking with CPI for this calculation.

Here, then, is the source data for my scatter plot:

|

| Graph #2: Quarterly Growth of RGDP (blue) and the Inflation-Adjusted Federal Funds Rate (red) |

The graph runs from 1953 (before the FEDFUNDS data starts) to the end of 2008. I'll trim it down a little more in Excel when I can see the data.

On second thought, I'll grab all of the data for download, in case I have a use for it.

To see the path of the data but eliminate the jiggies, I'm figuring Hodrick-Prescott values for the two data sets. My objective is to preserve the "shape" of the data but make that shape more readable. So my smoothing constants are low, non-standard values. Here are the smoothed data (red) and the original values (gray):

|

| Graph #3: Smoothing the Real FEDFUNDS data |

Graph #3 shows the interest rate. The source data is gray. The smoothed data is red. The value of the smoothing constant is 4, as the legend indicates. The same details apply to Graph #4:

|

| Graph #4: Smoothing the RGDP data |

I put the two smoothed series together in a scatterplot, with GDP on the horizontal and interest on the vertical. Tried to make the dots pretty. Connected them with thin gray lines. And added a linear trend line, in black. Here is the result:

|

| Graph #5: RGDP and the Real FedFunds Rate with a Linear Trend Line (smoothed data) |

The RGDP values shown on the horizontal axis are for quarterly data. The center of the dot cluster (call it the average growth rate) appears to be somewhere between 0.5 and 1.0. It's a low number because it is a quarterly rate. Annual rates would be, ballpark, four times bigger. That would give an average real growth rate between 2% and 4% per year, which sounds about right.

The straight black trend line tilts upward to the right. Doesn't look like much, but it probably slopes

more than you think. The trendline formula says the slope is 0.4876. That's almost 0.5. If the slope was 0.5, Y would go up by half of X, and the trend line would go up six inches for each foot it goes to the right. That's almost as steep as a flight of stairs. Steeper than it looks.

For some reason whenever I see a trend line on a scatterplot, the trend line is straight. A glance at the scattered dots should tell you there's no chance the trend is a straight line. But straight-line trends are

commonly used on scatterplots. Maybe that has to do with the way economists think.

I made a copy of Graph #5 and changed the trend line to something other than a straight line, just to see how it looks. It looks like Poirot's moustache:

|

| Graph #6: RGDP and the Real FedFunds Rate with a Polynomial Trend Line |

The trend line is in the same place, and it still slopes up to the right. But along the way, it curves up and down. I can't tell you much of what those curves might mean, but I can tell you the trend is not a straight line.

I wanted a better look at changes in the scatterplot trend. I thought I might split the cluster down the middle, and get a trendline for each half. Then I got bold and decided to split economic growth into four overlapping subsets so I could see four overlapping trend lines.

I inserted four new columns into the spreadsheet, alongside the smoothed data. I used formulas to put values into these columns, based on growth rate limits I picked for each subset. This gave me the values in chronological order, with blank cells where the values were outside the limits.

Then I made a scatterplot, and it was garbage. Excel doesn't do what I expect when there are blank cells intermixed with the values. But I didn't know that yet. So I tried again. This time I subsetted the interest rate data instead of the growth rates.

This time, all the blank cells were interpreted as zero values. I got a whole lot of dots at the zero level, and I couldn't get rid of them. That's when I figured out the blank cells must be the problem.

The question then was how to convert one column of numbers into four columns based on specified value limits, without having blank cells mixed in with the data. The answer of course was VBA.

I wrote a routine to arrange the data in a way that satisfied both Excel and myself, and at last I got a look at the trends of the subsetted data:

|

| Graph #7: The Scatter Data split out as Low Growth, High Growth, and Intermediate Levels |

I got four overlapping trend lines. These lines occupy the same general location as the overall trend line shown on Graph #5. The trend lines, taken together, show a positive correlation similar to the overall trend: lower on the left, higher on the right. However, three of these four trend lines are downsloping. They show

negative correlation. They contradict the overall trend, and they contradict Richard Werner.

After a pointless argument with myself that lasted much too long, I decided to write more VBA, to subset the scatter data on interest rate values this time rather than growth rate values.

The code writer complained that he already did the work and why should he have to do it again. The econ hobbyist pointed out that the central bank changes the interest rate on purpose, so the interest rate subsets must be more informative than the growth rate subsets and the code writer should have known which data to subset the first time around. The code writer gave us the finger. But he eventually admitted that his outrage was no more than a way to postpone the inevitable. The matter was finally settled when the blogger pointed out that he had to stop blogging so that the code writing could commence.

I looked at Graph #7 and divided up the vertical axis to make four overlapping groups. Then I copied the code I used to make Graph #7 and tweaked it for #8. The code revision took less time than the argument.

Here's what I got:

|

| Graph #8: The Scatter Data split out as Low, High, and two Intermediate Interest Rate Ranges |

This time, three of the four subsets show positive correlation. One shows negative.

I don't know, though. Take the high and low trendlines on Graph #8 and throw them away. Keep the two in the middle. They point

up. The space between these two trendlines appears to be the same space where we find all four trendlines of Graph #7. But three of those four trendlines are pointing

down. It looks like you could get any result you want, if you pick the right dots.

Something is wrong here. The trend is what it is. We must be doing something wrong if we can make the trend slope this way and that. We must be doing something very wrong.

I think I know what the problem is: The trends we've created here are long-run trends. They reduce more than half a century to only "up" or "down". (The correlation is positive, not negative, Werner says.) Yes, we cut off the data at the crisis. Yes, we stripped away the inflation. But too much variation remains in our fifty-plus years of dots and data. Too much for one trend line. We still have the golden age, early on. And though we removed inflation, we still have the multiple recessions that occurred at the time of the Great Inflation. Then we have the changes in policy that began around 1980, and the change in the trend of interest rates from uphill to downhill. And we have the gradual but persistent slowing of economic growth for the full extent of our fifty-plus years. These factors and others throw monkey wrenches at our scatterplot trend.

I think we need shorter trends. We need to evaluate shorter time periods. To answer the obvious questions (How short? Where shall we start them and stop them? How can we justify our choices?) consider the data we are evaluating: It is economic growth, and the interest rates which may or may not affect that growth. It makes sense, I think, to base our time periods on the business cycle.

No, you know what? Between one recession and the next there is sometimes a low point of growth. Sometimes more than one low point. To shorten and simplify trend segments in the scatter, our subsets can stop at every low point. So let's not say business cycles. Let's say growth cycles instead -- or, not even cycles, but loops. Growth loops. That's it, growth loops.

I dug up an old spreadsheet and plugged in the data we've been developing here. Changed a few graph titles and some range names. Put Xs in the MinGrowth column at the low points of growth. And clicked a couple buttons to get some graphs. Here is the first one:

|

| Graph #9: The Business Cycle of 1957-1960 |

Against a background showing the whole scatterplot, the graph highlights the data points of the period identified in the subtitle line. The first dot of the series is green and the rest are red. Red lines connect the highlighted dots in chronological order.

The black trend line for the highlighted dots shows a positive correlation (higher on the right) as Richard Werner says. But, oddly, what happens with the dots seems to contradict Werner. After the first three dots (green, red, red) the dots start to go higher, meaning the interest rate was rising. The horizontal distance between the dots gets smaller, meaning increases in the growth rate are getting smaller. Then, after the rightmost red dot, the RGDP growth rate falls as the dots step to the left.

Based on the data values shown here, interest rate increases after the third quarter of 1958 appear to have caused economic growth to slow. The story these dots tell matches the central bank narrative that Richard Werner rejects.

The trend line displays the positive correlation that Werner points out, but the dots behave as the central bank describes. The dots are saying that Werner's positive correlation is not relevant.

By the way... The same RGDP and the same real interest rate for the same dates we see on Graph #9, but without the smoothing the HP calculation provides, looks like this:

|

| Graph #10: Same Data as Graph #9, but Without the Smoothing |

A growth loop of sorts is still visible here, in red. But it's not the same. The smoothed data definitely makes the shape more visible. But if you want to say that I have not preserved the shape of the unsmoothed data, I refer you to Graphs #3 and #4.

The trend line for this unsmoothed data is high on the right, as for the smoothed data.What the dots have to say is less clear. But at low interest rates growth is increasing; rising rates put a halt to the increase; and high interest rates leave us with reduced growth. The dots reiterate the central bank narrative, despite the positive correlation shown by the trend line.

Not every smoothed growth loop has a trend line that agrees and dots that disagree with Werner, as the first one does. Many of them show small clusters or tight groups, and are difficult to read at all. Some of these might make better sense if combined with an adjacent growth loop. I didn't look into that.

I made 16 subsets of the "smoothed data" scatterplot. The subsets run from low to low of the smoothed RGDP growth rate, with the lows sometimes at recessions and sometimes between recessions. On each graph, the green dot indicates the start of the subset. The last of the red dots, then, becomes the green dot of the next graph. Here are all 16 subsets:

|

| Graph #11: The 16 Subsets (MinGrowth to MinGrowth) of the Scatter |

|

I could tell less by looking at the graphs than I expected. So I made a table listing the start date, end date, and slope of each subset, noted some features for each subset, and got total counts for each feature. Here's the table:

Sixteen subsets total. Half of them slope up to the right (positive correlation) and half slope down to the right (negative correlation). The average of all 16 slope values is -0.342, an overall negative correlation that stands in contradiction to the positive correlation Richard Werner finds in his scatter plots.

(Note that the positive correlation Werner finds in his scatterplots, like the trend line he does not draw, is based on the whole set of dots, not on sequential subsets of the dots. A trend line based on the whole collection by design ignores the economic forces that put any one dot in a different position than the preceding dot. It ignores economic forces, while pretending that economic forces are best described by the data set as a whole.

This problem arises not only here, but also with the

Phillips curve and

Okun's law. Anyone who bothers to look will discover the shapes and behaviors visible in sequential subsets of these datasets.)

The average of the negative slope values is -1.391, about twice as far from zero as the average of the positive slope values, which happens to be 0.707. (Oddly, too, the slope of the 1997Q4-2001Q2 period is 1.414.)

For the whole 16 subsets, I count nine that support the central bank narrative, where a rising interest rate is associated with slowing economic growth. The relation is sometimes concurrent and sometimes sequential. For the whole 16 I count five that contradict the central bank narrative, either a falling interest rate associated with slowing growth, or a rising rate with rising growth. I count two subsets which neither support nor contradict the narrative.

Of the nine subsets that support the central bank narrative, four show a positive and five a negative trend slope. Of the five that do not support the narrative, three show positive and two show negative slope.

I could not resist splitting the 16 subsets into "first 8" and "last 8". The first half ends and the second half begins with 1980Q2. The first half runs 22½ years, if my fingers were up to the counting of it, and the second half 26½ years. From start to finish, each half has nine growth minimums. Okay, that makes sense, as the subsets begin and end at growth minimums.

For the first half, the average slope of the trend lines is 0.265. For the second half, -0.949. For the first half, there are six positive and two negative slopes. For the second half, just the reverse. For the first half, a rising interest rate leads to slowing growth 6 times out of 8. For the second half, 3 times. For the first half, a rising interest rate leads to rising growth once. For the second half, a falling interest rate leads to slowing growth four times.

That's all the stats I have.

Conclusion? Policy may not be as simple as "By lowering rates, central banks accelerate growth and by raising rates, they slow it." But central banks surely do not have it all wrong.

// Files

RGDP and Real Fedfunds.xls for graphs 3 thru 8

Looking for Loops in RGDP and Real FedFunds.xls for graphs 9 and 11

Looking for Loops (omit smoothing).xls for graph 10

{kind=link}