From Bloomberg View:

Decade of Fiscal Stimulus Yields Nothing but Debt: Caroline Baum

By Caroline Baum Aug 4, 2011 8:00 PM ET

When George W. Bush took up residence in the White House in January 2001, total U.S. debt stood at $5.95 trillion. Last week it was $14.3 trillion, with $2.4 trillion freshly authorized by Congress Tuesday.

Ten years and $8.35 trillion later, what do we have to show for this decade of deficit spending? A glut of unoccupied homes, unemployment exceeding 9 percent, a stalled economy and a huge mountain of debt. Real gross domestic product growth averaged 1.6 percent from the first quarter of 2001 through the second quarter of 2011.

Facts. Not all the facts, but facts. What is it they say? The first step is admitting you have a problem.By Caroline Baum Aug 4, 2011 8:00 PM ET

When George W. Bush took up residence in the White House in January 2001, total U.S. debt stood at $5.95 trillion. Last week it was $14.3 trillion, with $2.4 trillion freshly authorized by Congress Tuesday.

Ten years and $8.35 trillion later, what do we have to show for this decade of deficit spending? A glut of unoccupied homes, unemployment exceeding 9 percent, a stalled economy and a huge mountain of debt. Real gross domestic product growth averaged 1.6 percent from the first quarter of 2001 through the second quarter of 2011.

My solution is different from everybody else's solution. Most especially, it is different from those solutions that propose cuts to government spending. But my solution does not depend on avoiding the facts.

From USNews:

Obama Taxes, Debt, and Stimulus Worked, Trumping GOP Blather

By John Aloysius Farrell

Posted: February 3, 2010

But, OK, the Obama tax cuts and stimulus package did exacerbate the debt problem that he inherited from the Tom DeLay generation of Republicans--which dropped the pay-as-you-go policies of the Clinton-Gingrich years to finance two wars and the biggest expansion of Medicare since LBJ with the government credit card.

And, due to the failure of the Democratic message machine (from smugness, or maybe just exhaustion), the need for the new red ink that the Bush-Obama rescue packages added to the national debt was poorly explained, went undefended, and became an invitation for Republican demagoguery.

But it is not that the GOP has offered any better ideas.

Partisan bickering. Sadly, the strongest argument here is blame. And the best excuse is that "the need" to add to the national debt was "poorly explained".By John Aloysius Farrell

Posted: February 3, 2010

But, OK, the Obama tax cuts and stimulus package did exacerbate the debt problem that he inherited from the Tom DeLay generation of Republicans--which dropped the pay-as-you-go policies of the Clinton-Gingrich years to finance two wars and the biggest expansion of Medicare since LBJ with the government credit card.

And, due to the failure of the Democratic message machine (from smugness, or maybe just exhaustion), the need for the new red ink that the Bush-Obama rescue packages added to the national debt was poorly explained, went undefended, and became an invitation for Republican demagoguery.

But it is not that the GOP has offered any better ideas.

But the $8.35 trillion we added to the national debt in the last ten years did not leave us better off than we were before. So it would take one hell of a good talker to convince people of the need to add even more to the national debt.

My view is that our economy does not grow because private debt is excessive. And, that this problem is not resolved by raising or lowering the public debt.

From Vox:

Deflation, debt, and economic stimulus

Richard Wood

3 March 2011

Under Policy A the central bank creates new currency to purchase government bonds on the secondary market. The principal purpose is to finance a rise in bond prices and lower interest rates and, thereby, stimulate private investment.

Considerable risks and side-effects could arise from the continued application of this policy in the current environment of historically low interest rates.

If the consumption/investment preferences of bond holders are unchanged, then, under Policy A, bondholders may simply purchase new domestic bonds (or other close substitutes) with the newly created currency received from the central bank, or they may purchase higher yielding foreign bonds/assets offshore. On this basis, the additional money supply would not go directly, if at all, to domestic consumers, wage-earners, the unemployed, or to non-finance businesses – the areas where it is most needed to generate widespread domestic demand growth.

Quantitative easing -- Policy A -- does not ease the maladjustment of income that creates toxic assets by making liabilities toxic. The additional money supply does not go to domestic consumers, wage-earners, the unemployed, or to non-financial businesses – the areas where it is most needed.Richard Wood

3 March 2011

Under Policy A the central bank creates new currency to purchase government bonds on the secondary market. The principal purpose is to finance a rise in bond prices and lower interest rates and, thereby, stimulate private investment.

Considerable risks and side-effects could arise from the continued application of this policy in the current environment of historically low interest rates.

If the consumption/investment preferences of bond holders are unchanged, then, under Policy A, bondholders may simply purchase new domestic bonds (or other close substitutes) with the newly created currency received from the central bank, or they may purchase higher yielding foreign bonds/assets offshore. On this basis, the additional money supply would not go directly, if at all, to domestic consumers, wage-earners, the unemployed, or to non-finance businesses – the areas where it is most needed to generate widespread domestic demand growth.

And why is money "most needed" in these areas? Because that is where the toxic liabilities are. If we print money and use it to pay off debt for consumers, wage-earners, and the unemployed, we eliminate those liabilities. We eliminate that debt. We free up the economy so it can grow again.

And how does it grow? Because the money you have, your income, becomes discretionary again. You don't have to use so much of it for debt service. So you can use more of your income like you used to, to buy stuff. That is what stimulates the economy.

From The Hill:

Dems call for stimulus in debt deal as CBO offers warnings

By Erik Wasson - 06/22/11 08:19 PM ET

Senate Democrats on Wednesday said stimulus measures should be included in a debt-ceiling deal even as a new Congressional Budget Office (CBO) report shows public debt surging to nearly twice the economy’s size by 2035.

Sen. Charles Schumer (D-N.Y.) and other Democrats said the slowing economy demands a deficit-reduction package that includes provisions to create jobs.

The thing that bothers conservatives most about liberal policies, I think, is that liberal policies lead to what Rush Limbaugh has called "the aggrandizement" of government. Liberal policies make government bigger. That doesn't bother liberals, so they always miss the biggest objections that conservatives have to their views.By Erik Wasson - 06/22/11 08:19 PM ET

Senate Democrats on Wednesday said stimulus measures should be included in a debt-ceiling deal even as a new Congressional Budget Office (CBO) report shows public debt surging to nearly twice the economy’s size by 2035.

Sen. Charles Schumer (D-N.Y.) and other Democrats said the slowing economy demands a deficit-reduction package that includes provisions to create jobs.

Quantitative easing creates new money and puts it in the hands of the wealthy; we tried this and it has not fixed the problem. Stimulus measures circulate new money into the hands of the poor, but do it in a way that conservatives object to.

If we print money and use it to pay off debt for poor people, the rich people get paid. So why should they object? And the poor people get debt relief, which is what we need to get the economy going again. And the government is not "aggrandized" in any way.

From Bloomberg Businessweek, January 14, 2010:

After the Stimulus Binge, a Debt Hangover

Trillions of dollars have been spent keeping the global economy afloat. But now fears about the Great Recession are giving way to worries about something else: The Great Reckoning

By William Pesek

Government policymakers from Washington to Tokyo are tallying the bill for last year's stimulus binge, and the results won't be pretty for investors or elected officials. Since the collapse of Lehman Brothers in September 2008, the Group of 20 largest industrialized economies have spent more than $2.2 trillion—much of it borrowed—trying to restore growth.

If the problem is excessive private debt, why would you even try to solve the problem by increasing public debt? But that's what we do.Trillions of dollars have been spent keeping the global economy afloat. But now fears about the Great Recession are giving way to worries about something else: The Great Reckoning

By William Pesek

Government policymakers from Washington to Tokyo are tallying the bill for last year's stimulus binge, and the results won't be pretty for investors or elected officials. Since the collapse of Lehman Brothers in September 2008, the Group of 20 largest industrialized economies have spent more than $2.2 trillion—much of it borrowed—trying to restore growth.

If you print a dollar and use it to pay off debt, the debt and the dollar cancel each other out, and both of them disappear.

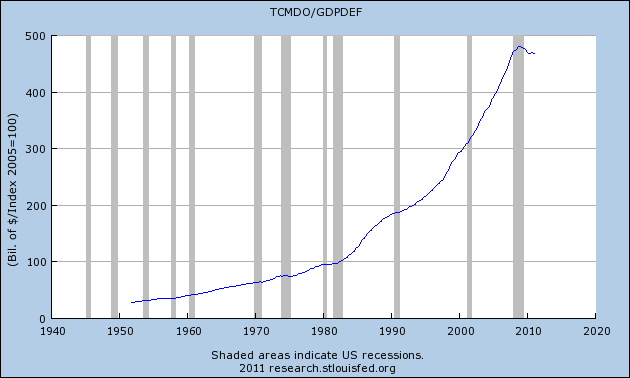

Or maybe, if fractional-reserve banking turns a dollar of money into $10 of debt, then we can print a dollar and use it to pay off $10 of debt. Or if each dollar supports $35 of debt, then maybe we can print a dollar and use it to pay off lots of debt. And if paying off debt destroys the dollar, then this plan is not even inflationary.