You know the economy is a mess. Everybody knows. What does it mean?

It means the people making the policies and the people that give them guidance are wrong. That's what it means. And how did they get to be wrong? Well, there are two stories about this. I'll tell the short story first:

Keynes died.

End of story. Samuelson and the rest of 'em came along then, and started making things up and calling them Keynesian things. But they were not Keynesian things. They were

Samuelsonian things, and like that. The economy was in a golden age in those years after Keynes died, the years after World War II, and no matter what Samuelson and the rest of them did, it worked. It wasn't that they were good. They were just lucky.

After a while their luck ran out, because the magic dissipated, whatever magic it was that had created a golden age. So then, there started to be bad consequences from the things they were doing and the things they had done. Frankly, they did not know what to do. They threw their hands up, and puzzled it.

Which brings us to the second story.

It happened the same way mythology and fables developed: People like Lucas and them started telling each other stories. The good stories, they repeated. The bad stories, they forgot. They repeated the good stories and expanded upon them, and more storytellers joined in the tell. And they called the story DSGE and they kept telling it right up to the moment that the economy went into depression. They keep telling it, even now.

That's the end of the second story.

"Meme". I think that's the word. It's like a virus in society, or in a group like a group of economists, say. And all you need is one wrong phrase in the right place, and nobody notices, and the story grows and becomes like a Bible, and people just accept it, and nobody even notices the parts that are wrong.

Keynes said, "It is astonishing what foolish things one can temporarily believe if one thinks too long alone." It is true, to be sure. But it is equally true that one may think foolish things because one thinks too much in the company of others, and the meme spreads like measles, spreads like the plague.

I spend a lot of time being wrong, and I'm slow-moving. It can't be helped. But I do my best to avoid repeating clever phrases other people come up with. I won't use an idea unless I understand it my own way, see that it is right, and have it in my own words.

The title of this post is taken from

the post I'm evaluating, from Rodger Malcolm Mitchell's place. Rodger has a whole long list of "Ideas You May Enjoy" and this one fascinated me. The title fascinated me. The post, not so much.

Rodger, I should say up front, I don't want to be mean. I'll try to offer constructive criticism. But I think you're telling stories, Rodger, bad stories. I think you're trying to create memes like Lucas did, false notions well told that catch on and spread. And I won't have it, Rodger. I won't have it.

You don't want to be responsible for the sort of embedded errors that Lucas is responsible for, do you Rodger? I hope not. But your work is full of errors.

So, the post. Rodger writes:

The Fed raises interest rates to fight inflation. To fight recession, the Fed does the opposite. It cuts interest rates.

This may sound logical except for one, very small detail. The opposite of inflation is not recession. The opposite of inflation is deflation. So doing the opposite of what you would do to counter inflation makes no sense when trying to counter a recession.

One of the things that messed up Samuelson and them, in the 1960s, was the Phillips Curve. Economists at the wheel at the time described a tradeoff between inflation and unemployment, a tradeoff that was disputed by other economists riding shotgun. And when, in the 1970s, we ended up with high inflation and high unemployment *both* (rather than one high and the other low) there was a Chinese fire drill and a change of drivers. Lucas took the wheel.

But it is not a question of whether inflation and recession are opposites. Rodger Malcolm Mitchell misunderstands the simplest thing. He leaves out

spending.

Inflation is associated with "too much" spending. Recession is associated with "too little" spending. The Fed raises or lowers interest rates to influence the level of spending, to guide the economy on a "best path" between inflation and recession.

If you must reduce the logic to "opposites," Rodger, too much spending and too little spending

are opposites. Therefore, raising interest rates or "doing the opposite" does make sense.

In fact I should prefer to say that raising and lowering interest rates DID make sense in the 1950s and 1960s. It does not make sense any more, or at least it does not *work* any more, because the economy has changed since those days: We use far more credit now than we did then, per dollar of spending. And because our use of credit is vastly greater, the influence of changing interest rates is vastly greater.

In an economy that uses credit for growth, changing interest costs affect growth. In an economy that uses credit for everything, changing interest costs affect everything.

In an economy that uses credit for growth, changing interest costs affect growth. In an economy that uses credit for everything, changing interest costs affect everything.

Rodger writes:

The history of Fed rate cuts, as a way to stimulate the economy, is not a good one.

The economy's response to interest rate cuts has changed because our use of credit is vastly greater. If interest rates now were half what they were then, but our reliance on credit had doubled,

there would be no reduction of aggregate interest cost. In fact, as long as people still held loans issued at older, higher interest rates, total interest costs would be higher now, despite the low rates.

And that does not even begin to consider the downpressure on the quantity of money resulting from the repayment of all that principal. Nor does it consider the reduction of discretionary income remaining after the loan payments are made. Nor does it consider that a change in interest rates today affects not only the decision to expand the business, but also the cost of borrowing to meet payroll.

So, Rodger, if monetary policy doesn't work as well as it once did, there are reasons for that. But there is *no* sweeping generalization to be made, that (as you say) "doing the opposite of what you would do to counter inflation makes no sense when trying to counter a recession". That is a bad meme, Rodger, a bad virus. Like the Mad Cow, it harms the brain. Stay away from it.

Next, Rodger does some fuzzy math:

Why does popular faith hold that cutting interest rates stimulates the economy? Because popular faith views only one side of the equation. For each dollar borrowed a dollar is lent. $B = $L. That much is trivial.

Cutting interest rates does cost borrowers less. So, the theory is, a business needing $100 million would be more likely to borrow if interest rates are low than when they are high. Further, consumers are more likely to spend when borrowing is less costly. So making borrowing less costly stimulates business growth and consumer buying. At least, that is the theory.

What seems to be ignored is the lending side of the equation. When interest rates are low, lenders receive less money. And who are the lenders? Businesses and consumers.

You are a lender when you buy a CD or a bond, or put money into your savings account. When interest rates are low, you receive less money, which means you have less money to spend on goods and service — which means less stimulus for the economy.

In short, interest rates flow through the economy, with some people and businesses paying and some receiving. Domestically, it’s a zero-sum game.

Here Rodger expresses one of the things I really don't understand about MMT people. They are often quick to make the distinction between the Federal sector and the rest of us. But they refuse to pry apart the Non-Federal sector and examine the

growing imbalances within it.

Changing interest rates, Rodger says, and increases or decreases in borrowing, is all "a zero-sum game". Like MMT, Rodger refuses to look at the effect such changes have on the relative positions of the financial sector and other components of the Non-Federal sector.

Rodger suggests that interest income is just like the rest of income. That is comparable to saying

wages are just like profits. I trust you find that notion laughable.

I am the greatest fan of aggregates, by the way. Accumulated totals. I think this is the right way to look at the macro-economy. But the failure to break out subtotals and look at the changing balances between different sectors, is a mistake. It is a mistake that leaves one ignorant of powerful economic trends.

And then what happens is, there is a financial crisis and all you can say is, "I didn't see it coming."

Rodger says:

What seems to be ignored is the lending side of the equation. When interest rates are low, lenders receive less money. And who are the lenders? Businesses and consumers.

As if the borrower and the lender are the same person. The same person on both sides of the transaction. No, I don't see that. I'm not borrowing more or borrowing less from myself, depending on interest rates. That's ridiculous. I'm borrowing from someone who has the money to lend.

But suppose I was borrowing from myself. Suppose we all were. For each of us, our interest cost and our interest income would go up equally. But if we want to save, we are liable to leave a portion of our interest income in savings. This reduces our spendable income, necessitating an increase in borrowing. Thus our interest costs rise, as does our interest income. As does the portion we wish to leave in savings, which again necessitates an increase in borrowing...

Or if another MMT view is true -- "loans create deposits" -- then I'm not borrowing

from anyone. The money I borrow is created by the act of borrowing. In that case there is really no lender. So then, business and consumers are not the lenders, despite what Rodger says. But suppose we say the financial sector is the lender. Then the gain from the lending accrues to the financial sector, further skewing imbalances within the Non-Federal sector, the imbalances that Rodger and MMT refuse to examine.

You may wish to point out that employees of the financial sector are members of the non-financial sector. I will grant you that. But I would remind you that the operating expenses of the Federal Reserve amount to

only about 5% of its income. And that for lesser banks, expenses are

apparently even less. Thus only a tiny fraction of financial-sector income must end up "spent back into circulation" outside the financial sector. Except for the Fed, of course.

I'm not sure I accept the view that loans create deposits. But if Rodger does, then he contradicts himself. For interest is not a zero-sum game. It is an imbalance generator, further skewing imbalances within the Non-Federal sector. And the only way *not* to see it, is to refuse to look.

You are a lender when you buy a CD or a bond, or put money into your savings account. When interest rates are low, you receive less money, which means you have less money to spend on goods and service — which means less stimulus for the economy.

Rodger assumes that all of interest income is withdrawn from savings and spent into circulation. Yet surely, some of the interest income gets rolled right back over into new savings. How much? I don't know. For the sake of argument, say half. So then, only half the money paid in interest circulates back into the economy as money.

The other half circulates back as credit-in-use. That drives up the aggregate annual interest payment required,

even if there is no change to interest rates. It also reduces the quantity of money in circulation, interest-free money in circulation. It makes the Debt-per-Dollar ratio higher by increasing the numerator *and* by decreasing the denominator.

I know: Nobody looks at the

DPD ratio but me. That doesn't make it irrelevant.

Rodger writes:

A growing economy requires a growing supply of money. Cutting interest rates does not add money to the economy. That is why there is no historical correlation between interest rates and economic growth. During periods of high rates, GDP growth is not inhibited. During periods of low rates, GDP growth is not stimulated.

Has Rodger never heard of the return on investment? If a businessman can earn more by leaving his money in the bank than by sinking it into his business, he is liable to do just that. Cutting interest rates makes a given rate of profit more attractive, and stimulates business activity.

Actually, this is the solution to the problem of excessive reliance on credit. Let the return to the rentier be so low that he prefers productive activity. Today, however, we think of this solution as a "liquidity trap."

Yes, absolutely, a growing economy requires a growing supply of money. And no, cutting interest rates does not directly add money to the economy. It does so indirectly, by inducing an increase of borrowing. At least, before the crisis it did.

And as for Rodger's claim that "there is no historical correlation" between interest rates and growth, well, that is the idea he presents in the title of his post, proposing to show the correlation is a fallacy. In the excerpt, Rodger states his view as fact. But that does not make it a fact. Rodger asserts his hypothesis. Truth by proclamation.

Anyway,

I think Sidney Homer would not agree that there is no correlation.

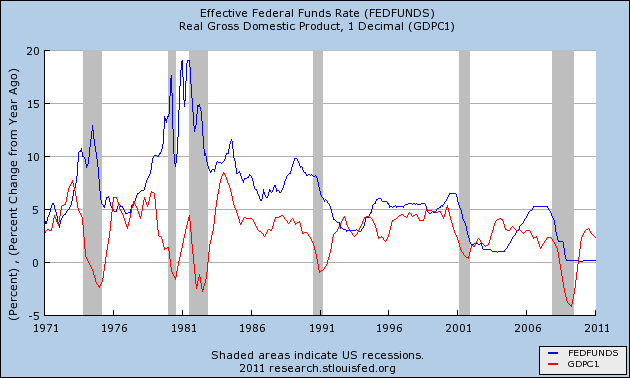

The claim that high interest rates do not inhibit growth, nor low rates encourage it, is an interesting hypothesis. It leads directly to Rodger's graph, which I reproduce here:

You can see from the blue line that rising interest rates did inhibit growth by creating the recessions of 1974 and 1980 and 1982.

Rodger describes the graph:

Blue is interest rates. Red is GDP growth. Not only are low interest rates not associated with high economic growth, but to a slight degree the opposite seems to be true. There seems to be a small correlation between high interest rates and high GDP growth.

I'm not gonna argue the fine points here. Let me point out simply that Rodger's graph begins in 1971, which is just about the end of the good years of the post-WWII period. So, Rodger's graph is a study mostly of the bad years. If you want to make the economy good, it helps to look at the difference between good times and bad. You cannot ignore the good years.

Been down so long it looks like up to me is not good economics.

I looked at what FRED has on this. Rodger could have taken the graph back to 1954. I'm thinking, if the good years supported his argument he would have shown them. But he didn't show them.

Oh, and Rodger's graph shows nominal GDP, not real GDP. So it doesn't really even show growth. Really, it shows inflation.That's why Rodger's red GDP line is up over 10% there in the 1970s. We didn't have growth like that. We had

inflation like that.