Tweaked a little, this is a re-post from 14 September 2014.

Back in February 2014 I came across this graph at

The Current Moment:

|

| Graph #1 |

Also this one, which they called "Doug Henwood's Graph":

|

| Graph #2 |

Both graphs show productivity. The one graph compares productivity to compensation; the other compares it to wages. Wages and compensation both lag productivity. But compensation lags less than wages, because compensation (as the source site explains) is

wages plus benefits.

I find it useful when people provide background information like that. But that's not what caught my eye. It's the difference in separation points that caught my eye: On Graph #1 the "wages" line breaks away from the productivity line suddenly, just around 1974. On Graph #2 the "compensation" line breaks away from the productivity line gradually, but much earlier -- possibly as early as 1960.

This difference fascinates me. For if the failure to keep up with productivity is a problem, these graphs show it is a problem that became obvious around 1974, but began much earlier.

If it is a problem we want to solve, then we must be clear on the causes. Clearly, those causes were operative

before the 1970s. If we only look in the 1970s for the causes, we will likely find false causes.

I did notice that the first graph is indexed "relative to 1970" while the second is "rebased to 1960". In other words, by design, the lines on Graph #1 meet at 1970 and the lines on Graph #2 meet at 1960. The indexing (or the choice of a "base year") influences the location of the break-away point on the graphs and changes the impression we get from the graphs. I think we are hoodwinked by the indexing.

On Graph #1 in particular, between 1955 and 1975, it's pretty clear that the orange line is going up faster than the red line. If you could take the whole red line and just move it down a little bit, you might make the two lines meet at just one point. That point might be 1956. If you looked at that version of the graph, you would see real wages falling behind productivity since 1956.

I don't know which is more disturbing -- the 1956 start, or the false impression created by indexing.

The second graph, Henwood's graph, seems to show compensation falling behind productivity since about 1960. But since it doesn't show earlier data, it leaves the door open. 1956 could still be the more accurate date.

I followed the

Current Moment link back to Doug Henwood's and liked what I found there. I emailed Henwood:

Hi. I recently came upon an old page (2001) at Left Business Observer

http://www.leftbusinessobserver.com/Stats_earns.html

I'd like to use your "productivity and compensation" graph on my blog. The page says I should get permission first, so I'm asking.

All the similar graphs that I've seen focus on the separation beginning mid-1970s. Your graph shows the separation beginning much earlier. It was eye-opening for me.

"Heavens," Henwood replied. "I have much more recent versions of that - let me find one for you tomorrow." He did, too:

.png) |

| Graph #3 |

"Here's the latest," he wrote. "Haven't updated it since November, but it's through the third quarter of last year. 'Compensation' includes fringe benefits - since much of that is health insurance, much of the real value is eaten up by medical inflation. Direct pay is pay without fringe benefits. All are inflation-adjusted and indexed so the base year = 100."

The three lines on this graph combine the three different series shown on the first two graphs above. In addition, on Graph #3 the series are indexed to 1964. And -- don't you know it! -- the break-away point this time looks to be 1964 at the latest.

A little over a week ago -- it seems much longer -- I was reading a discussion

at Reddit. The topic was "What might actually be holding back workers’ wages".

Somebody blamed Reaganomics. One guy, I'll call him Joe, rejected that idea: "Your idiotic blaming of Reaganomics would be dependent on Reaganomics traveling back in time a decade and starting the trend in the mid 70's," Joe said.

I love it. That's one of my themes: You can't just blame the guy you don't like, especially if the things you're blaming him for happened before his turn at bat. Reminds me of a Mike Kimel quote that

Jazzbumpa has in his sidebar:

#15 Time moves in a single direction.

No doubt.

Anyway, Joe provided a link to a "productivity and real wages" graph -- the same graph from

The Current Moment that I have as Graph #1 above. Small world.

I complimented Joe on the graph. But then I went off-topic, so much that Joe had to disagree with me. I pointed out that the graph is indexed "relative to 1970". I said:

If the graph was indexed relative to 1956 we would see the slowing of wages begin in the mid-1950s, then see the gap widen more quickly since the mid-1970s.

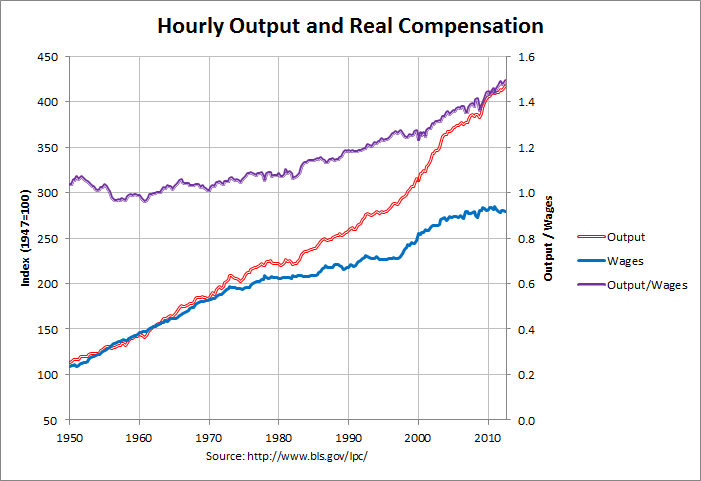

Joe replied: "That is not how the graph would change changing the index year at all. Here is one indexed to 1947. There is still a trend starting at 1970 where wages and output are decoupled."

He showed this graph:

Yes, the red and blue lines are comparable to those in the graphs above. Yes, the base year is 1947 this time. And yes, the red and blue run much closer before 1974 than after. However, the trend of hourly output increases faster than wages since the mid-1950s on Joe's graph. The failure of wages to keep up with productivity begins in the mid-1950s.

This graph has a third line -- the purple line -- that shows a ratio of the red and blue. Nice! I was going to show the ratio.

The purple line shows how productivity ("hourly output") is changing relative to wages. If you look at the purple line you can see the trend changes from downward to upward around 1956 or 1957. That means productivity started gaining on wages around 1956 or 1957. I think Joe was hoodwinked by the indexing on Graph #1.

Wages started falling behind productivity around 1956 or 1957. So if you want to blame Reaganomics... or if you want to blame Jimmy Carter or Gerald Ford or Richard Nixon or Lyndon Johnson -- or John F. Kennedy for that matter -- to do it you will have to make time go in the wrong direction. You'll be breaking Rule #15.

The failure of wages and compensation to keep up with productivity is a problem that began in the 1950s.

Yesterday, at

The State of Working America I found this graph from the Economic Policy Institute:

It is similar to the graphs above. Since the 1950s, the dark blue "productivity" line goes up faster than the light blue "compensation" line. But the indexing has the two lines tangled together early, so you don't notice compensation falling behind until the mid-1970s.

This graph is important because it comes with

this data. (Excel XLSX, 37KB) So of course I took the file, uploaded it to Zoho, and customized it for on-line use.

The on-line spreadsheet let you "take the whole red line and just move it down a little bit". All you do is pick the year that you want to see the lines meet, and

enter that four-digit year into the yellow cell on the spreadsheet. The graph changes so that the lines meet at the year you specify.

I'm deleting the on-line Zoho spreadsheet from this post because it makes the screen jump. Instead of showing you the blog page from the top, it jumps straight to the spreadsheet. They fix that bug every time I tell 'em about it, but the bug keeps coming back. I give up.

The spreadsheet is available in the

original (Sept 2014) post. Here's what it looks like:

.png)

{kind=link}

{kind=link}