|

| Interest Rate and Simulation |

George Lucas might not agree, but if you want to design economic policy you need to create a simulation of the economy in a spreadsheet. Your simulation needn't exactly duplicate each twist and turn of every real-world variable, but it has to be a decent facsimile. And the calculations that produce the numbers for your "sim" have to be based on real-world economic forces. Otherwise it's not a simulation, it's a fantasy.

Robert Lucas, I mean.

//

In that Noahpinion post I was railing about the other day, Noah links to The Leverage Cycle (PDF, 58 pages) by John Geanakoplos.

I've come across Geanakoplos before. I like his thinking. I checked out Noah's link. This detail from the PDF stuck in my head:

In standard economic theory, the equilibrium of supply and demand determines the interest rate on loans.

That makes sense. I thought it was more complicated. Now I want to look at it. Maybe I can come up with a calculation of real-world factors that give me numbers I can use to simulate an interest rate. For the simulation I've been wanting to create since Jimmy Carter was President.

No rush.

Design

I did the following graphs and worked out the calculations already once this morning, taking notes. I'll do it all again now, hopefully a little more organized and presentable.

To simulate the interest rate, I want to base my calculation on the years before inflation became a problem. So when I design the calc I won't look at data after 1965.

I wanted to start right after World War Two, but some of the data doesn't start until the end of 1951. That's okay. It's good, actually, because it gets me past the Fed-Treasury Accord.

I want to ignore the recessions and the changes in policy intended to create or to recover from recessions. I think that will give me a smoother simulated path of interest rates. I can already imagine that rates go up (due to the demand for loans) until rising rates cause recession, and then falling rates allow the decline in borrowing to bottom out and then increase again. I don't need to complicate the sim calc with all of that. Not yet, at least.

Similarly, I want to ignore inflation. Solved a lot of that problem just by stopping at 1965.

And then I want to look at consumer debt, changes in consumer debt, as a measure of the demand for new credit. (Existing debt is the measure of demand for total credit in use.) I'm thinking interest rates pretty much move in sync, for consumers and for everybody else. And I have data I can use for consumers. And this is a first effort. I can revise the thing later, if I get bigger ideas.

So I've got the price of credit (the interest rate) and I've got the demand for credit (consumer debt), and I've got nothing for the supply of credit. That's okay. I'm assuming the supply is constant (or, growing at a constant rate). That's what I get by ignoring policy responses to inflation and recession. And come to think of it, ignoring such unusual moments is probably what John Geanakoplos meant by "the equilibrium of supply and demand".

If I have success simulating the interest rate while ignoring supply, I can still try to improve it later by looking at supply.

So that's the plan.

Development

For an interest rate I figured I'd use the Federal Funds rate. But at FRED the FEDFUNDS rate only goes back to 1954. So I got the "3-Month Treasury Bill: Secondary Market Rate" instead. That goes back to 1934 and runs real close to FEDFUNDS since '54. Should be good. Here's what I'm thinking:

|

| Graph #1: The Price of Credit -- The Interest Rate |

That will be my test: I figure a "sim" interest rate based on the years 1952 to 1965. Then, using that calculation, I extend the line out all the way to 2016. If my sim line goes crazy, I wasted my time figuring and you wasted your time reading (unless you're just here for the laughs). But if my simulated interest rate seems to follow the actual interest rate, then I'll be happy with my calculation. And I'll be one step closer to actually creating a simulation of the economy on a spreadsheet.

(I know: Other people have probably done that already. No problem. I get satisfaction from trying to do it, and more satisfaction if I succeed.)

So that's the interest rate. The "price" of credit. I looked next at the "demand" component, consumer debt. (For now I'm taking "supply" as given, remember.) First, the quarterly change in consumer debt:

|

| Graph #2: Quarterly Change in Consumer Debt |

I rejected Graph #2 at a glance. It shows instability in the last three years of the 1960s, to my eye, but doesn't show increase until the 1970s. By contrast, the price of credit -- Graph #1 -- shows increase right from the start. From 1950. Persistent increase. Graph #2 does not show the growth of demand for credit that would be needed to generate the increase visible on Graph #1.

I changed Graph #2 to show the quarterly change as a percent of GDP. That made it worse: higher in the mid-1950s than the mid-1960s. It should have been low early and high later. And the downslope from 1964 to 1967 was more sharply down -- down, just when inflation was picking up. It was exactly wrong.

I thought: I need to multiply it by something that shows increase. I knew immediately then what to bring in to the calculation: accumulated consumer debt, relative to GDP. I revised the calculation, and put it on the same graph with the interest rate from Graph #1:

|

| Graph #3: The Interest Rate (blue) and my Calculation (red) |

|

| Graph #4: My Calculation (red) Sized to Fit the Interest Rate |

The sim does appear to fall apart by 1965. I think what I'm seeing is the blue line rising with inflation, and the red line not. But remember I said that I'm "ignoring policy responses to inflation and recession." I should expect to see the red and blue lines separate while inflation is building. So I'm not disappointed.

Come to think of it, while inflation is building the "erosion" of debt is increasing. Perhaps this accounts for the apparent downtrends in the red line from 1965 to 1970 and 1973-1975 or so.

These same influences likely cause the "wiggles" of the mid- and latter-1950s, noted above. Those wiggles may not be so big a problem as I thought.

I made a copy of Graph #4 and marked it up to show where the two lines run together. I count six locations:

|

| Graph #5: Copy of Previous Graph with the Stitching Highlighted |

I'm pretty happy with my calculation.

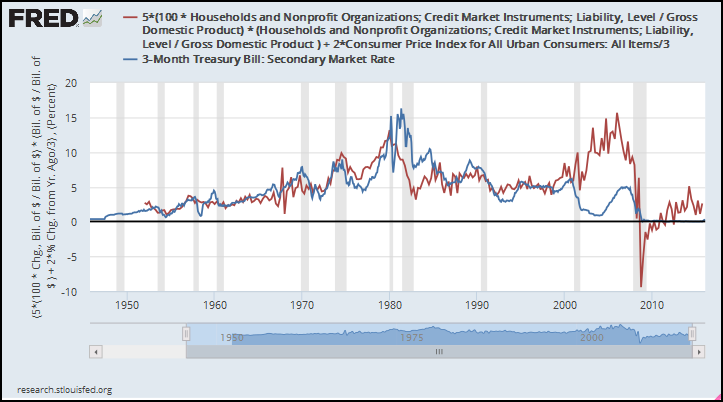

Graphs #4 and #5 end in 1980. I moved the end-date to 2016 to see the whole picture. The half-dozen "stitch" points still exist in the years before 1980. In addition, you can see that the red and blue lines run together for about five years in the 1980s and for most of the 1990s:

|

| Graph #6: Copy of Graph #4 Extended Into 2016 |

From the start to the year 2000 -- almost 50 years -- the two lines run together, with disturbances that appear to arise largely as effects of inflation. After 2000 it's a different story. But before 2000 the result is promising.

I don't think my calculation is useful for a simulation of interest rates as it stands. I'm wondering how it will look if I include the inflation rate in the calculation.

|

| Graph #7: Added Two-Thirds of the Inflation Rate, and Revised the Size Adjustment |

The Last Years

The years after 2000 deserve another look.

Before I added inflation into the calculation (see Graph #6) the calculated line (red) runs consistently at or below the blue line, till 2000. After 2000 the red line runs significantly higher than the blue, to the crisis.

On closer look, I see the red line starts to go high in 1998. Whatever date you pick, the change from "at or below the blue" to "above the blue" is unusual because the red line does not run above the blue until that date. There was a change, I'm saying -- a change in the economy.

The red line, my simulation of the interest rate, is based on the real-world relation of debt to GDP. The red line going high is a result of debt going high, unusually high in those years. You remember that.

If my calculation provides a good simulation, then maybe what it shows in the years after 1998 is right. If the simulation is good, maybe it shows that interest rates should have been higher in those years, higher than they actually were. In other words: interest rates were too low for too long.

Remarkable, huh?

Then, after imagining interest rates as high in the 2000s as actual rates were in 1981, the simulation shows interest rates going negative. My graph, based on debt and GDP, shows a sudden need for negative interest rates. That's something Paul Krugman was saying:

Early on in this crisis I and quite a few other economists — but not enough! — declared that we had entered a classic liquidity trap. This is a situation in which even a zero short-term interest rate isn’t low enough ...

The economy, Krugman was saying, needed negative interest rates. Like Krugman, my interest rate simulation wants negative rates.

More recently then, the simulation has rates in positive territory again.

John Taylor:

I’m saying if they had a strategy in place that would have seen interest rates moving up in 2011 or 2012, but not a lot, then I think things would be working better.

The simulation shows rates positive and increasing in 2011 and 2012.

Look: I don't think my interest-rate simulation is perfect. Adding the inflation rate to it is a fudge factor. But with or without that fudge factor, the simulation produces conclusions similar to Krugman's conclusions. And it indicates the same patterns of interest rate behavior as the Taylor Rule.

For the record, I don't claim to be a fan of the Taylor Rule. But I get similar results. Looking at consumer debt in this way

change-in-debt-as-a-percent-of-GDP * the-accumulated-debt-to-GDP-ratio

I get the same result that John Taylor gets when he looks at actual inflation and desired inflation and the equilibrium real interest rate and GDP and potential GDP and whatever else he stuffed into his rule.

The interest rate simulation presented here emerges from debt-to-GDP ratios. What the simulation shows is that you can arrive at Taylor Rule conclusions simply by looking at consumer debt and GDP.

// Update 18 March 2016: For another example of combining levels and rates in a calculation, see my Levels and Growth Rates of Debt and Income from last October.

6 comments:

I do not think interest rates were too low for too long. I certainly do not think we needed record high rates in the 2000s.

What I think is the calculation shows debt was extremely high and GDP was lagging in the 2000s, pushing the sim number way high. The problem is not that interest rates were too low.

The problem was that there was too much debt.

Here's a clip from Ben Bernanke's blog at Brookings, from April of last year.

Ben says "the Fed's interest-rate policies in 2003-2005 can't explain the size, timing, or global nature of the housing bubble."

I'm saying consumer debt explains most of that.

Bernanke's blog post:

The Taylor Rule: A benchmark for monetary policy?

http://www.brookings.edu/blogs/ben-bernanke/posts/2015/04/28-taylor-rule-monetary-policy

Art

I do not know if this helps you find what you are looking for but, you can calculate and implied equation for the 3-month Treasury bill yield as a function of liquidity preference: I = EXP(4.27 – 45.5*M/PY) where M= Monetary Base and PY is Nominal GPD.

You get a pretty good fit.

Son of a gun!

Thanks Oilfield

I don't know either if I can use it... I haven't planned that far ahead. But I do like to see things like that. The calculation gives something like a smoothed trend line for the interest rate.

When you think the only economic variables involved are GDP and base money, well, it has to make a person stop and think.

Thanks!

Oh like this old post! Maybe I can make the simulation values less jiggy by using smoothed (hodrick-prescott) values in place of the values I used.

Post a Comment