I need to write my next post. I'm tempted to respond to Noah, either Occult Mysteries of the Heterodox or The Folk Theory of business cycles. But responding to either one would likely drag me into something other than what I do, which is to try and understand the economy.

I ended up at Noah's "folk theory" post, still undecided about what to write. Accidentally left my mouse pointer on the picture at top of his post and something came up:

Derp? What's derp?

Oh, foolish and stupid. Of course.

I'm gonna respond to the "folk theory" post. And I'm gonna do my damnedest to make Noah look derp.

Noah's opening:

A lot of people seem to subscribe to what I call the Folk Theory of business cycles (not to be confused with the Folk Theorem of game theory). Roughly speaking, this is the idea that:

1. Debt growth is necessary for GDP growth.

2. As GDP grows, debt levels become too large, leading to an economic crash.

3. Therefore, booms cause busts, through the mechanism of debt accumulation.

1. Debt growth is necessary for GDP growth.

2. As GDP grows, debt levels become too large, leading to an economic crash.

3. Therefore, booms cause busts, through the mechanism of debt accumulation.

Noah calls it a theory of business cycles. But when I read the three points he gives, I see the cycle that reaches crisis in 1929 and then not again until 2008 or so, a long cycle. It has been called a debt supercycle. I think that's a good call.

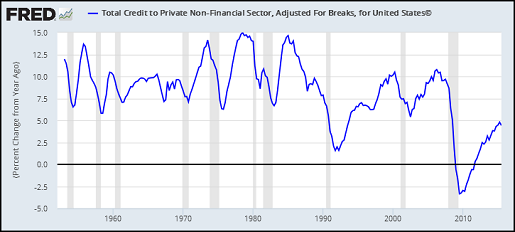

If you look at percent change in private non-financial debt

|

| Graph #1 |

The bottoms are closely related to end-of-recession. But the tops are only loosely related to start-of-recession. If you tell me a recession ended today, I can tell you borrowing will increase tomorrow. But if you tell me borrowing started to decrease today, I cannot tell you we'll have a recession tomorrow. I cannot.

I can't read business cycles in the tea leaves of debt. But I can read the major cycles. Look at the debt in billions instead of as percent change values:

|

| Graph #2 |

This is the cycle I'm talking about. BANG the Great Depression. And then nothing but debt growth for 75 years give or take and then BANG the Great Recession. That's not the "business cycle". That's a "long wave" or a financial cycle of some kind.

You know, if Noah is taking some serious financial-cycle, debt-theory stuff and pretending it applies to the ordinary business cycle, he's doing straw man work, misrepresenting an argument so that the argument makes no sense, so it is easy to shoot the argument down. After he shoots down the debt theory applied to business cycles, absent theory he can generalize and satisfy to himself that the debt theory doesn't apply, ever.

I won't stand for it.

//

In the section of Noah's post called "The Illusion of Knowledge" we read:

Suppose, for the sake of argument only, that debt had nothing to do with economic cycles. Suppose it was only along for the ride - when they're more economic activity, people borrow and lend more with each other, and when growth slows down they borrow and lend less, but the activity of borrowing and lending has no effect on how much gets produced. In this hypothetical fantasy world, we'd naturally see debt levels rise most of the time, but we'd see them fall temporarily when there's an economic downturn. In other words, we'd see exactly what's on the graph above. But rising debt levels would be no cause for alarm.

Holy crap. Noah has us assume that debt has nothing to do with the business cycle. And then, debt levels are "no cause for alarm". He's assuming the conclusion he wants us to reach.

//

Listen to what Noah says about prediction:

If you can't use a theory to make concrete predictions, what good is the theory?

Oh my god, if I wrote something like that I would be SO embarrassed.

Myself, I use "theory" to understand the economy. You need predictions if you are trying to make money, in the stock market for example. A person who wants to understand the economy and understand the economic problem so that the problem can be fixed, you don't need prediction for that.

There's a quote from somebody famous, I don't remember who, and I'll probably bungle the quote, but it goes something like this: We study the past in order to understand the present so we can improve the future. Something like that.

That's what theory is good for, Noah.

Derp.

//

In the "Bad Policy Advice" section of Noah's bad post, he really gets under my skin:

... my third problem with the Folk Theory of business cycles is the biggest: I suspect that it encourages bad policy. The story the Folk Theory tells is that you can't have good economic times without increasing debt, and that increasing debt always causes a bust. So good times come at a price - you can't have prosperity today without disaster tomorrow.

Bad policy? I think it's a bad policy to reject a theory without understanding it, and then present an embarrassingly simplistic version of the theory as if that's really the theory. Here:

The story the Folk Theory tells is that you can't have good economic times without increasing debt, and that increasing debt always causes a bust.

That's more or less what you can see in a graph, if you bother to look at one. Those are the facts. But to grab those simple facts and pretend they form a whole causal explanation, well that's just another straw man.

Instead of looking for the whole causal explanation -- like I do on my blog -- Noah sums it up with some moralistic bullshit. Here:

So good times come at a price - you can't have prosperity today without disaster tomorrow.

And then he has the nerve to complain about the morality tale, as if it wasn't he, Noah, who had presented it:

... a morality tale, rooted in partial-equilibrium thinking - if you borrow and consume too much today, you will be sad when you have to pay it back... When we think of the economy as a morality play, it encourages bad policy.

Noah is moralizing about moralizing about debt!

//

What do we need from economists?

If we need anything, we need them to tell us how to fix the economy. To explain the problem in a way that makes sense, so that we can see our way out of the problem. That's what we need from economists.

We don't need economists to take other people's ideas and simplify the ideas down to where they are wrong and then point out the wrong ideas as if these were the ideas of those other people.

And we don't need economists to moralize about moralizing -- or about anything.

//

Here, Dick. You have to understand that the problem with debt is cost. There is a benefit from using debt, but there is also a cost. If we increase our use of debt for 75 years, and increase it enough to offset the cost of the debt we're accumulating all the while, at some point the shit is gonna hit the fan.

The shit doesn't have to hit the fan. But you have to understand that it will, unless we do something to prevent it. This is where "thinking" comes in. That's the part Noah doesn't cover in the post.

Oh, and you can have good economic times without increasing debt. We can't, because policymakers think we can't, and they set up policy accordingly. But we can, if policy will allow it.

2 comments:

This statement right here;

"Suppose it was only along for the ride - when they're more economic activity, people borrow and lend more with each other, and when growth slows down they borrow and lend less"

gives up the ghost as far as Im concerned. There is this persistent notion amongst mainstream economists that private debt is just Greg borrowing from Art. You can substitute "bank" for Art if Art is a net saver so the story goes. The story is flawed.... fatally.

People going into debt with debt with banks is not the same as them going into debt with each other. If I borrow a 1000$ form you, that is 1000$ you cant spend. If I borrow a 1000$ from a bank that does not limit their future lending in nearly the same way.

First off banks wouldn't have 1000$ more to spend if I didn't borrow it and secondly when they evaluate my loan worthiness the only place they look is at me, not in their vaults.

These guys are hopeless Ive decided

"These guys are hopeless Ive decided"

I'm starting to focus more on criticizing the pros -- Noah, Summers, Sumner ...

I find it satisfying, and maybe I can learn something along the way.

As far as Noah's "Folk Theory of business cycles" goes, I couldn't let it go because he is basically saying that my views are foolish and stupid. Of course, it's not my views, really. He has taken the analysis of debt and dumbed it down to 1-2-3 and turned it into garbage. And he attributes the garbage to people like me.

It still burns me!

Post a Comment