A review of "A Rehabilitation of Monetary Policy in the 1950s" by Christina D. Romer and David H. Romer. The paper is from The AEA Papers and Proceedings, May 2002. (Link to PDF)

OVERVIEW:

The PDF is well-organized, brief (7 pages) and quite convincing. The authors note that Federal Reserve policy before the 1980s is not well regarded by modern economists. The article holds that 1950s policy is comparable to modern policy, while policy of the '60s and '70s is not. The article offers "a rehabilitation" of the modern view of 1950s Fed policy.

WELL-ORGANIZED:

Here are the opening sentences from the first three paragraphs of the article:

American monetary policy in the 1950's has typically not been judged favorably. These unfavorable judgments seem strangely at odds with economic performance in this decade. This paper suggests an alternative view of monetary policy in the 1950's, and hence a possible solution to the mystery of that decade's outstanding economic performance.They fit together exceptionally well.

Each paragraph expands upon its opening sentence. The first identifies critics and criticisms of 1950s policy. The second identifies economic performance criteria and performance achieved. The third outlines the organization of the balance of the paper.

The balance of the paper follows that outline, even down to the detail of using header lines with outline-style numbering. These are the headings:

The paper also includes one table, two figures, five footnotes, and over a dozen references.

- Narrative Evidence

- An Overarching Concern about Inflation

- Model of the Economy

- Implementation of Policy

- Statistical Evidence

- Specification

- Results

- Conclusion

BOLDNESS

The paper presents the myopic and egotistical view that '50s policy was right because it is comparable to modern policy. This view is presented more than once.

The authors write: "We show that policy in the 1950's was actually quite sophisticated." They do not say "actually quite sophisticated by present standards;" but that is clearly what they mean. Those Neanderthal economists of the '50s were darned near as good as we are, dear.

They do not say "the policy of the 1950s was surprisingly sophisticated," which would have expressed surprise. They say policy was "actually quite sophisticated." The words actually quite seem to suggest arrogance rather than surprise -- as if coming from a position of modern superiority.

The authors write of "unquestionably good economic performance" and "outstanding economic performance" to describe the 1950s. There is a backwash effect from this: They were outstanding. And they are actually almost quite as good as we sweet moderns. So we are outstanding, too. QED.

The authors write: "Their model of how the macroeconomy operated contained ... a remarkably modern view of the causes of inflation...." And the article praises the 1950s for its "sensible view" of full employment -- again meaning a view that seems sensible by present standards. The economic thinking of the 1950s is held to be almost as good as ours today: remarkably modern and sensible.

The authors also contrast 1950s policy to that of the 1960s and '70s. To the latter is attributed a "simplistic Keynesian model." This is mere taunting. The authors write:

"If monetary policymakers in the 1950's had figured out the essence of sensible policy, the mistakes of the 1960's and 1970's cannot just have been the result of continuing ineptitude or misunderstanding. Rather, something must have changed."This is really well-crafted stuff; the authors manage to align modern policy with the sensible 1950s, and at the same time jab a finger in the eye of the 1960s and '70s.

I hesitate to offer this particular criticism of the paper. For it is not economics to say: They are good, for they are sensible, like us. Nor is it economics to say: They are not good, for they are different and simplistic. This is not economics at all. Yet it seems somehow to have become part of modern economics. So I point out the flaw.

At no point in the article is it suggested that present-day economic conditions are excellent; only that present policy is. But how can policy be good, when it produces an economy such as ours? Financial crisis, recession, debt, unemployment, inflation, and lethargic growth. The egotistical vision of present policy as the best of all possible worlds is a major flaw in the paper.

If Romer and Romer want to say the policies of the 1950s are similar to those of recent times, all well and good. But they assume present policies are right, and they compare '50s policy to this modern perfection. It would be funny, if economic conditions today didn't create such problems for so many people.

EVIDENCE SELECTION

The authors gather interest-rate data from two sources: from Citibase, as far back as 1954; and for older data they took an old graph and guesstimated what the numbers must have been. (The authors call it "deducing the numbers from the graph.")

But then, it's not as bad as it sounds, because they ignore half of their guesstimated numbers. The authors note that for their 1950s data they take the period including only 1952 through 1958. Seven years out of ten. They explain:

We start two years into the decade because the Federal Reserve was unable to pursue independent monetary policy until the Treasury-Federal Reserve Accord of 1951. We stop at the end of 1958 for reasons discussed below.

The data doesn't show what they need it to show in 1959, so they dropped that year from their calculations!

1959 is omitted from the Table 1 calculations, because it makes their bad statistical evidence look even worse. Include that bit of data, and the evidence fails to support the claims made in the article. The weight on inflation is estimated imprecisely enough as it is, the authors note, and

Furthermore ... if one continues the estimation through 1959 the estimated coefficient on inflation falls considerably and is measured even more imprecisely.

Note that if the weight falls "considerably," it no longer supports the view that anti-inflation policy was vigorous in the 1950s. If it falls from 1.178 to anything less than 1.0, it no longer indicates that the Fed raised real interest rates in response to inflation.

Stopping at 1958 concerns me much more than starting at 1952. The "reasons discussed below" turn out to be that including 1959 would have made the authors' claims look false. But this hardly seems to matter, as the authors boldly assert

Empirical analysis of the behavior of the funds rate shows that policymakers in the 1950's responded much more aggressively to expected inflation than did policymakers in the 1960's and 1970's.

That's an unsupported claim, given the imprecision and the careful selection of both statistical and narrative evidence to obtain the desired result.

WEAK LINKS

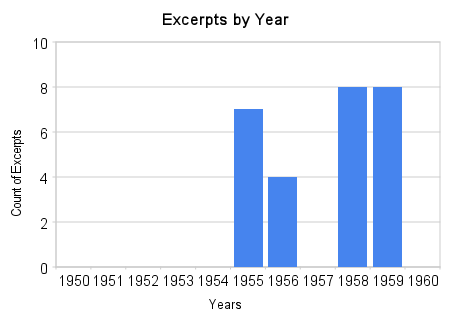

The narrative evidence consists of a bunch of excerpts -- 27, by my count -- mostly from the Minutes of the Federal Open Market Committee.

it is hard to test statistically whether the Federal Reserve of the 1950's was blessed with good sense or good luck. For this reason, it is most useful to analyze narrative evidence.

So they analyze 27 excerpts selected from ten years of Minutes of Federal Reserve meetings. "The overarching concern about inflation is revealed most clearly," they write, "... during the times when inflation began to accelerate ... in the mid and late 1950's."

They consider 11 excerpts from the mid 1950s and 16 from the late 1950s. Not one from 1957. None from 1954, 1953, 1952, 1951, or 1950. Surely if the concern was "overarching" the Fed must have been just as concerned about inflation when prices were stable as when prices were rising. Surely also, one could find 27 or more strong statements of concern about inflation from Federal Reserve members during the 1970s, when inflation was heading into double-digits. The narrative evidence is suspect on these grounds alone.

One reason the article is convincing is that it arouses nostalgia. The excerpts recall mysterious and memorable names like Watrous Irons and William McChesney Martin. Of course, you cannot base an economic argument upon nostalgia.

You cannot base one on narrative excerpts either, as the authors point out: "To see if policymakers backed up their words with actions, one needs to supplement the narrative analysis with statistical evidence."

The statistical evidence uses "regression" and the "Taylor rule" to compare monetary policy decisions of four time periods -- the '50s, the late '60s and '70s, the '80s, and the '90s.

The "Taylor rule" calculation combines output and inflation performance data to calculate an interest rate. This rate is considered (by economists) to be a target for monetary policy: The Federal Reserve simply aims for that interest rate target, and all is then right with the world. (The Taylor rule itself is a remarkable product of modern egonomics. See this post for more.)

The authors do some really nifty arithmetic: The article claims that monetary policy was tougher on inflation in the 1950s than in the '60s and '70s. The argument is simple: If the "weight" is greater in the 1950s, then the policy was tougher. The logic is elegant.

However, they admit that

"The weight on expected inflation is estimated less precisely in the 1950s than in other decades"In other words, their evidence is not precise. The authors refer the reader to "the narrative evidence presented in Section I" to make their case. Our statistical evidence is junk, they tell us. So here, look at the cherry-picked quotes we showed you above.

Oh -- and for the record: Their calculated "weight on expected inflation" in the 1950s is 1.178 with an "error" factor of 0.876. The error value is 74% of the weight value. That's a mighty big margin of error. The phrase "less precise" doesn't do it justice.

Their calculated weight on output is also "very imprecisely estimated."

The narrative evidence makes a nice story. But it is only one of many possible stories we could find in a selective summary of a ten-year collection of statements. A different selection of narrative evidence could easily support a completely different conclusion. The narrative evidence is weak.

As the authors note, "One needs to supplement the narrative analysis with statistical evidence."

But the statistical evidence is also weak: "Because the 1950's sample period is inherently limited and the variability of inflation in this decade is small" -- that, yes, and the bad weight estimates, and the careful selection of evidence -- "this empirical analysis must be viewed as a suggestive check on the narrative analysis rather than as a conclusive test."

The statistical evidence is inconclusive, and the authors refer more than once to the narrative to strengthen their case. The argument presented -- by the current head of the Council of Economic Advisers -- is based on the principle that a chain with two weak links is somehow better than a chain with one.

MY CONCLUSIONS

1. The article's conclusion states: "Monetary policymakers of the 1950s had a deep-seated dislike of inflation and acted to control it." I'm willing to accept that view. But nowhere in the paper is the correctness of the policy actions evaluated. The policies are simply assumed to be good because we like them.

In 2002 when the article was published, modern policy was assumed to be good. Six years later we found out different. And then Christina Romer became the Chair of the Council of Economic Advisers. But things are amiss here, and good science is lacking.

2. William McChesney Martin was head of the Fed from 1951 to 1970: the '50s and the '60s. But according to the Romers, policy was good in the '50s and bad in the '60s. So what happened? Martin's brilliance in the 1950s suddenly turned into ineptitude and misunderstanding? Oh, oh, oh, the model of the economy changed, they say. William McChesney Martin must have adopted "a naive Keynesian model" and abandoned his "overarching concern about inflation."

I don't buy the argument.

3. The Taylor rule can be used to calculate an interest rate target. But this does not mean that the whole concept of monetary policy as implemented today is correct. The calculation works like the Holodeck on Star Trek -- or like any computer program: The outputs are only as good as the assumptions allow. Garbage in, garbage out.

The Taylor rule produces a number that economists think should be the right number, based on their incomplete and flawed understanding of the economy. Confidence in the Taylor rule presupposes that the modern understanding of economic forces is accurate and complete.

4. I am suspicious of the data omission. The authors omit not only 1959 from their survey, but also the first four years of the 1960s. Data points stop in 1958 and do not resume until 1964. That's a five-year stretch, ignored because at least one of the missing years throws off the results. I suspect the whole five-year stretch contradicts the article's view.

And as it happens, the omitted period is the key turning point noted in my 12-page PDF. I do not think this is coincidence. The facts of those years are not explained by the Romer paper. This failure of their explanation shows that some other explanation of inflation is needed.

1 comment:

For a brief review of the Romer & Romer paper see NBER:

http://www.nber.org/digest/jun02/w8800.html

Post a Comment