I gathered up the full set of RGDP quarterlies, 1947Q1 thru 2016Q4. Wrote up some VBA code to change Excel graphs. Set up a graph like I had for James Harrison's "good" and "slow" decades that we saw last time. And added recession bars to the graph.

(Later, I noticed the recession bars disappeared when I made gifs of the graphs. Oops.)

My intent is to examine business cycles one at a time, separate out the "growth phase" from the rest of the cycle, determine the growth rate for the growth phase, and consider the growth-phase growth rates for all the cycles together. I put a graph of the first business cycle on the worksheet and tweaked it to my heart's content.

Then I made a copy of the worksheet and started setting things up for the second business cycle. For each change I wanted to make, I figured out a way to do it in VBA. When the second graph was done, I had the code I needed to make the third graph, and the fourth, and the rest. I put a button on the worksheet to run the code.

Here is the process: I make a copy of the worksheet, rename the copy, click the button to run the code, and then erase a few "growth phase" values. That's all I have to do, and I have another graph done. Oh, plus I may have to revise the max and min values shown on the Y-axis. But that's it.

The trick is naming the sheet. My VBA code expects the worksheet name to be two four-digit-year values separated by a dash. When I click the button, the code uses the two dates to determine which data to show on the graph. It changes the title of the graph. And it initializes the "growth phase" column of the sheet.

All I have to do then is erase the first few "growth phase" values, and the last few, to shorten the red line on the graph until it shows only the growth phase. While erasing values, I watch the graph to check my work. Excel changes the graph automatically.

The growth-phase dates are self-revising. A worksheet calculation watches as values are erased from the "growth phase" column, and the dates adjust automatically. Those dates, and the RGDP dates taken from the worksheet tab, generate the graph title automatically. This prevents a lot of mistakes of a kind I'm very good at making.

(The recession bars, visible in Excel, make it easy to decide which values to erase and which to keep. Dunno why those gray bars disappeared from the gifs. The gray was too faint, maybe.)

My selection of the "growth phase" is seat-of-the-pants. There is nothing scientific about it. But with the way I have it set up, I could create all the graphs with the growth phase ending at the first possible moment, say, and create them all again with the growth phase ending at the last possible moment. Or whenever: Creating the graphs is not a stumbling block.

I get to think about the years I want to look at. And I get to decide what should be included in the growth phase. Excel and VBA between them take care of just about everything else.

Eleven graphs:

|  |  |

|  |  |

|  |  |

|  |

Taking the growth rate from each of the exponential trend equations...

Gathering the growth rate data, I was surprised to see a low number for the 1980s. I gave the graph a critical look, but everything was okay. And then I got a low number for the 1990s, too.

These are quarterly rates. Annual rates would be higher. That would help. But my growth rates for the 1980s and '90s are still lower than I expected, compared to rates in the 1970s.

Oh, yeah! That's what my previous post was about: If you only look at the growth phase of the business cycle, economic growth was strong in the 1970s. I didn't learn that lesson yet, apparently.

Here are all eleven "growth phase" growth rates from the tiny graphs above:

|

| Graph #12 |

Here is the 1980-1982 graph, showing a trend of 1.94% growth per quarter:

|

| Graph #13 |

|

| Graph #14 |

So the growth phase coming out of the 1980 recession was very short: just six months. The growth-phase growth rate is high because there was no period of moderating growth. After a six-month burst of growth the business cycle was suddenly in its transition phase, between growth and recession.

There was no period of gradual moderation after the initial burst of growth. As a result, the growth phase has a very high growth rate. We end up with a high point on the bar graph. So it looks like some kind of error.

Okay. Well, that accounts for the oddly high growth rate. But how about the low of 1953-1958?

It's a similar problem. There was a brief, sharp increase in RGDP coming out of the 1953-54 recession, and then, before long, a flattening. This time, though, the change was gradual rather than sudden. The change on the graph is not a sharp corner.

Originally, I thought about stopping the growth phase short. But I rejected the idea, assuming the flatness was moderating growth. So I included some of the "flat" growth in the data used to figure the exponential trend. That data is shown in red on this graph:

|

| Graph #15 |

Looking at the bar graph, I now see that the 1953-1958 growth rate should have been higher. So I realize that the flat growth must have been part of the transition phase between growth and recession. I should have excluded it from the growth phase. Here's the revised graph, with the red line appropriately pruned back:

|

| Graph #16 |

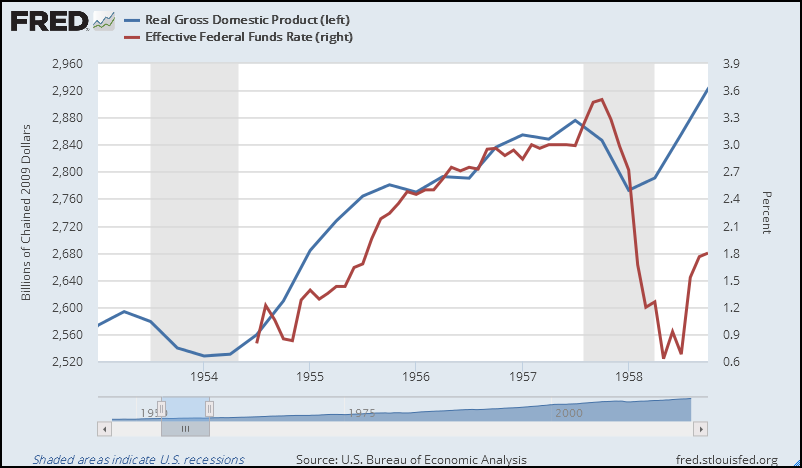

Here is RGDP (blue) for the same period (1953-1958) from FRED, along with the Federal Funds interest rate:

|

| Graph #17 |

Here is the bar graph, revised to show higher growth in the 1953-1958 period:

|

| Graph #18 |

The 1980-1982 value remains high, because I didn't change it. I don't know what would have happened if the Fed hadn't created the 1982 recession. (Well I do know: Growth would have tapered off gradually. The growth phase would have been longer, and the growth rate lower. But how much lower, I cannot say. I can only guess that it would fit the trend of decline visible in the other data on this bar graph.)

I won't revise the graph based on a guess. Nor will I consider the high value of the 1980-82 growth phase to be valid. In other words, I won't consider 1980-82 at all. I'll just omit it.

Given that, then, and converting quarterly growth rates to annual rates, this is the result:

|

| Graph #19 |

Myself, I would argue that growth-phase growth rates are a more telling indicator of economic health than business cycle growth rates. The growth-phase growth rate is growth at its best in each business cycle.

Coming out of recession, interest rates are low. Demand awaits fulfillment. And productivity is typically high, coming out of recession. These are features of the growth phase. So it provides a pretty good measure of the economy's "potential" (though that word has already been taken). Growth-phase growth shows our economy's performance is declining, and has been for a long time.

I bet you didn't see that coming.

Files:

RGDP & USREC (quarterly).xls (contains VBA code)

RGDP & USREC error checking & revisions.xls (contains VBA code)

Growth Phase Growth Rates.xls