Tripped over

an old post and found something I've been meaning to write about: good and bad debt. Here's

Arno Mong of Gang8:

Credit (and interest) is toxic only when it is spent unwisely, resulting in BAD (unpayable) debt. Debt is neutral both ethically and economically and not bad per se.

Debt is neutral, Arno says, and not bad

per se. But what happens if debt grows twice as fast as everything else? Is it still harmless, twice as big? Wait a bit then, and debt is four times times bigger than everything else. Wait a bit, and debt is eight times bigger. Wait a bit, and debt is 16 times bigger. Is it still harmless?

32 times bigger...

64 times bigger...

128 times bigger...

256 times bigger than everything else. Is it still harmless? I can keep this up longer than debt can continue not being a problem, I guarantee it.

It is not

the fact that there is such a thing as debt that is the problem. It's silly to say this could be a problem, though this is the problem Arno Mong evaluates when he says

debt is not bad per se. The problem with debt is cost. The cost of debt is the problem.

Mention the cost of debt, and everybody thinks of interest rates. Hardly anyone thinks of how much debt there is. Yet if interest rates fall by half and the accumulation of debt doubles in size, the cost of debt is not likely to fall significantly.

|

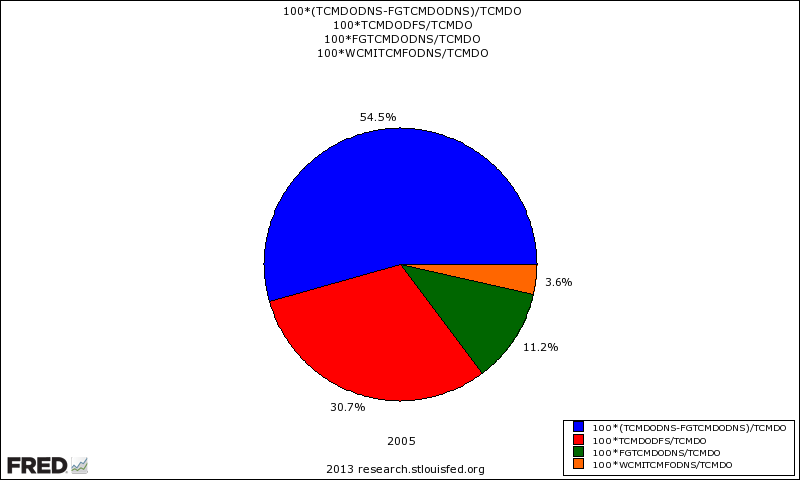

Graph #1 - Point of Interest: Monetary Interest Paid (red) is similar to

the Rate of Interest Multiplied by the Size of Total Debt (blue).

It is not obvious here that Interest Rates have been Falling since 1981 |

Again: It is the cost of debt that creates problems. Arno overlooks the fact.

As a philosophical concept, debt may be neutral both ethically and economically. But as a cost factor, debt is a problem that grows as it grows in size. Now, what else did Arno say?

"

Credit (and interest) is toxic only when it is spent unwisely, resulting in BAD (unpayable) debt."

Arno defines "bad" debt as "unpayable" debt. That strikes me as true, but based on a strictly limited meaning of the phrase "bad debt". It is not useful for evaluating the ideas I want to evaluate.

What is "bad" debt? It seems there are some people who identify debt as "bad" if it is government debt, and "good" if it isn't. That approach barely skims the surface. But maybe my method doesn't go much deeper: I just lump all the debt together and figure it's bad if there's too much of it.

Many people are not satisfied with such simple definitions. Steve Keen, for example, says it is

speculative debt that is bad. For Keen, speculative debt is unproductive.

Keen sees no problem with accumulating debt as long as that debt is for productive use, and not for speculation.

Moritz Schularick, on the other hand, thinks if you get a mortgage to buy a new house, that's okay, but if the house you're buying is a few years old, it's a problem.

If you're buying the house to live in, and there's not a trace of speculation in your soul?

No matter: If it's not a brand-new house, Schularick says, you're part of the problem. Because the new house is new production, and the older house is not.

Then there's Michael Leddy of

Orange Crate Art (not an economics site) who differs with both Keen and Schularick:

It is sad to say, but I’ll say it: Borrowing $64,000 to finance graduate work in the humanities is folly. Borrowing any amount of money to finance graduate work in the humanities is folly.

And in follow-up remarks:

People do borrow in sensible ways all the time (I think of the mortgage that went with our house), but for grad school in the humanities: not a good idea.

Mr. Leddy generally avoids economics on his blog. Even so, he has views on credit. In this case it appears he disagrees with Schularick on mortgages: Leddy does not say that "good" mortgage debt applies only to brand-new homes.

Finally, in comments on my

Cost Hinders Growth, Jazzbumpa (of

Retirement Blues and

Angry Bear) and an anonymous commenter ("Nonny") develop the analysis I want.

Nonny says that if the ratio of debt-to-GDP is stable, then

income (i.e. GDP) is being generated at a rate such that leverage remains unchanged. More ideally, leverage would decline. This pretty much defines the debate about productive vs unproductive debt.

By that measure, then, an increase in debt is "productive" if it leads to a proportional or greater increase in GDP.

Jazzbumpa points to the debt of the financial sector (as opposed to that of the productive sector) and says, "There is your unproductive debt."

Nonny wholeheartedly agrees, but suggests that

only that by looking more closely at nonfinancial debt accumulation , you can determine those periods when such debt was more or less productively used - by the "real" economy.

So, peel off the unproductive financial debt, and look for productive and unproductive in the non-financial debt. Makes sense.

Responding to my tentative effort to clarify the difference between "productive" and "unproductive" debt -- "good" and "bad" debt, presumably -- in follow-up comments Jazzbumpa says:

Debt to use in real investment is productive. Financial debt does not qualify.

Nonny takes it a step further,

to suggest that the most productive debt is for investments that can generate the income stream to pay off the debt. Debt used for consumption will raise GDP, and even create jobs if enough people are using debt to consume, but no income stream is generated for the debtors, so eventually they hit the wall. Still, even consumption debt generates GDP, so it's better than debt used for speculative finance, like Jazz says, which just redistributes GDP.

This is great. Now we have:

1. debt that increases GDP and pays for itself;

2. debt that increases GDP but does not pay for itself; and

3. debt that neither increases GDP nor pays for itself.

Now one can see depth in the difference between good debt and bad debt. I suppose we could add Arno Mong's "unpayable" debt as number 4 on that list. It works for me.

Suppose we apply this hierarchy of good and bad debt to the US economy, and take the measure of bad debt.

One way to look at it is Arno's way: unpayable debts.

That's the IRS way, too. I Googled

IRS bad debt data and found IRS

Topic 453:

If someone owes you money that you cannot collect, you may have a bad debt...

A business deducts its bad debts from gross income when figuring its taxable income.

The search also turned up a

Chapter 10 from the IRS, regarding business bad debts:

Business bad debts are mainly the result of credit sales to customers. Goods that have been sold, but not yet paid for, and services that have been performed, but not yet paid for, are recorded in your books as either accounts receivable or notes receivable. After a reasonable period of time, if you have tried to collect the amount due, but are unable to do so, the uncollectible part becomes a business bad debt.

The same search turned up this FRED graph of "bad debt expense":

|

| Graph #2: Bad Debt Reported on Corporate Income Tax Forms (I think) |

It's the first time I've looked at this graph, and I'm not comfortable with the long title FRED gives it. But it seems to make sense that this measure of bad debt from the IRS considers the bad debt reported on corporate tax forms. (As always, if you think I'm misinterpreting the graph, speak up.)

Okay, everything goes up. But how does "bad debt expense" compare to GDP?

|

| Graph #3: Bad Debt Expense as a Percent of GDP |

(The start- and end-dates on this graph differ from Graph #2 above.) Like Graph #2, Graph #3 shows a definite up-trend.

I need one more look at the "bad debt" corporate tax deduction -- this time relative to corporate profits:

|

| Graph #4: Bad Debt Expense as a Percent of Corporate Profits |

Graph #4 shows the same slow start as Graph #3. But this one is mostly below 10% before 1980, and mostly above 10% after 1980. And it shows a great immoderation in bad debt expense during the so-called Great Moderation.

These few FRED graphs show a definite long-term uptrend in bad debt expense. I don't suppose that surprises anyone, but I did have to see it for myself.

Bad debt expense. On our list of good and bad debt, it's Number Four: unpayables. The other three types of debt on our list all relate debt to GDP:

Type 1: down-trending debt, where GDP increases more quickly than debt;

Type 2: flat-trending debt, where GDP and debt increase at the same rate;

Type 3: up-trending debt, where GDP increases more slowly than debt.

For a first look at the debt-to-GDP ratio we can turn to the grandfather of debt productivity,

Grandfather Hodges. Under the heading

AMERICA'S DIMINISHED DEBT PRODUCTIVITY Hodges writes:

If America was more efficient in real productive employment of new debt, then less debt would be needed for each dollar of national income. But - - the reverse is true.

Less debt for each dollar of national income would mean the ratio was down-trending.

But the reverse is true: The ratio is up-trending. We're a Type 3 debtor nation. Our GDP (like our National Income) increases more slowly than our debt. Our debt increases faster than our income.

Grandfather Hodges says "We are less productive regarding debt than ever before." Hodges is saying that our debt -- our

total debt, not just the government's part -- is Type 3, up-trending debt. Our debt increases faster than GDP, now more than ever.

We are less productive regarding debt than ever before. Yup, that's what happens when you have up-trending, Type 3 debt.

Grandfather Hodges writes:

Each dollar of economic growth requires more debt per dollar than before - now over twice as much...

The left chart restates the above.

It shows that in 1957 there was $1.86 of outstanding debt for each dollar of national income.

But, today's economy needs $4.91 in outstanding debt for each dollar of national income.

That's 164% more outstanding debt load per dollar of national income.

That extra $3.05 of debt produced zero national income.

Hodges adds

if we look just at the period 2000 to 2010 total debt increased $30 trillion, while National Income increased but $4 trillion (GDP $4.6 trillion). In that period it took $7.50 in new debt to produce one extra $1 of added national income.

In a perfect world, less debt would be needed for each dollar of national income. But as Grandfather Hodges says, in our world the reverse is true.

More debt is needed for each dollar of national income. And this has been true since 1957, as Hodges shows. As his graph shows.

Well now wait a minute. That graph just goes up and up and up. There is what, one tiny little spot just before 1967 on the graph, where the line goes down for about 1/8 of an inch. That's the down-trend. That's the "good" debt -- that's *all* the good debt since 1957, by our definitions above. We got 1/8 of an inch of Type 1 debt, and that's it.

And then from 1967 to 1970 maybe, the graph is flat. Well, not really flat; looks like it goes up by one pixel. But call it flat. So the flat-trend, that's Type 2 debt, where GDP and debt increase at the same rate. This is the debt that doesn't pay for itself, but at least it helps GDP go up.

All told, then, Grandfather Hodges' graph shows five or six years when we had Type 1 or Type 2 debt. Five or six years out of the whole 1957-2010 period when we did not have "bad" debt, based on our definitions above.

This is problematic.

Our Types-of-Debt list is reasonable, right? How about Grandfather's graph; is it wrong? No, it's not wrong:

|

| Graph #6: TCMDO Debt relative to GDP (blue) and National Income (red) |

The list we came up with, the four different types of debt, that list is very comforting, you know? It helps us understand the world. Or it seems to. But Grandfather Hodges' graph turns everything up-side down. The debt-to-GDP ratio only goes up.

If the Grandfather Hodges graph is right, and if our list of the types of debt is right, then our debt, public and private, has almost always been a problem. It has almost always been unproductive, Type 3 debt.

That doesn't really seem right, does it. And it's

me saying it, the guy who always looks to debt first when there's a problem.

I know most people would rather be out of debt than in debt, but also, we all have our reasons for getting into debt. Is debt always unproductive? I think most people would say no. I think that's a good answer.

The graph is not wrong; debt goes up.

Out list of debt types is not wrong.

But we cannot interpret what the graph shows according to the list of types. How can this be?

I don't know. But here's what I think:

It's comforting to have a list like that, and it does make good sense. (I had a great time writing this post, working through Jazz and Nonny's comments, and coming up with that list of types of debt. I really did.) But it doesn't fit the data. It doesn't make sense when you look at the graph.

I know the graph is right.

I have to demote the list to a supporting role. A secondary role.

I'm left looking at a debt that is always growing faster than income, and I know it's a problem. I know not all that debt is unproductive; I know it in my heart. And I can't use the list to interpret that debt. So I have to demote the list to a tertiary role.

Ultimately, I'm left looking at all that debt, and I know it's a problem. So I say, just lump all the debt together, and figure it's bad when there's too much of it.

.gif)

.png)