I gathered up the full set of RGDP quarterlies, 1947Q1 thru 2016Q4. Wrote up some VBA code to change Excel graphs. Set up a graph like I had for James Harrison's "good" and "slow" decades that we saw last time. And added recession bars to the graph.

(Later, I noticed the recession bars disappeared when I made gifs of the graphs. Oops.)

My intent is to examine business cycles one at a time, separate out the "growth phase" from the rest of the cycle, determine the growth rate for the growth phase, and consider the growth-phase growth rates for all the cycles together. I put a graph of the first business cycle on the worksheet and tweaked it to my heart's content.

Then I made a copy of the worksheet and started setting things up for the second business cycle. For each change I wanted to make, I figured out a way to do it in VBA. When the second graph was done, I had the code I needed to make the third graph, and the fourth, and the rest. I put a button on the worksheet to run the code.

Here is the process: I make a copy of the worksheet, rename the copy, click the button to run the code, and then erase a few "growth phase" values. That's all I have to do, and I have another graph done. Oh, plus I may have to revise the max and min values shown on the Y-axis. But that's it.

The trick is naming the sheet. My VBA code expects the worksheet name to be two four-digit-year values separated by a dash. When I click the button, the code uses the two dates to determine which data to show on the graph. It changes the title of the graph. And it initializes the "growth phase" column of the sheet.

All I have to do then is erase the first few "growth phase" values, and the last few, to shorten the red line on the graph until it shows only the growth phase. While erasing values, I watch the graph to check my work. Excel changes the graph automatically.

The growth-phase dates are self-revising. A worksheet calculation watches as values are erased from the "growth phase" column, and the dates adjust automatically. Those dates, and the RGDP dates taken from the worksheet tab, generate the graph title automatically. This prevents a lot of mistakes of a kind I'm very good at making.

(The recession bars, visible in Excel, make it easy to decide which values to erase and which to keep. Dunno why those gray bars disappeared from the gifs. The gray was too faint, maybe.)

My selection of the "growth phase" is seat-of-the-pants. There is nothing scientific about it. But with the way I have it set up, I could create all the graphs with the growth phase ending at the first possible moment, say, and create them all again with the growth phase ending at the last possible moment. Or whenever: Creating the graphs is not a stumbling block.

I get to think about the years I want to look at. And I get to decide what should be included in the growth phase. Excel and VBA between them take care of just about everything else.

Eleven graphs:

|  |  |

|  |  |

|  |  |

|  |

Taking the growth rate from each of the exponential trend equations...

Gathering the growth rate data, I was surprised to see a low number for the 1980s. I gave the graph a critical look, but everything was okay. And then I got a low number for the 1990s, too.

These are quarterly rates. Annual rates would be higher. That would help. But my growth rates for the 1980s and '90s are still lower than I expected, compared to rates in the 1970s.

Oh, yeah! That's what my previous post was about: If you only look at the growth phase of the business cycle, economic growth was strong in the 1970s. I didn't learn that lesson yet, apparently.

Here are all eleven "growth phase" growth rates from the tiny graphs above:

|

| Graph #12 |

Here is the 1980-1982 graph, showing a trend of 1.94% growth per quarter:

|

| Graph #13 |

|

| Graph #14 |

So the growth phase coming out of the 1980 recession was very short: just six months. The growth-phase growth rate is high because there was no period of moderating growth. After a six-month burst of growth the business cycle was suddenly in its transition phase, between growth and recession.

There was no period of gradual moderation after the initial burst of growth. As a result, the growth phase has a very high growth rate. We end up with a high point on the bar graph. So it looks like some kind of error.

Okay. Well, that accounts for the oddly high growth rate. But how about the low of 1953-1958?

It's a similar problem. There was a brief, sharp increase in RGDP coming out of the 1953-54 recession, and then, before long, a flattening. This time, though, the change was gradual rather than sudden. The change on the graph is not a sharp corner.

Originally, I thought about stopping the growth phase short. But I rejected the idea, assuming the flatness was moderating growth. So I included some of the "flat" growth in the data used to figure the exponential trend. That data is shown in red on this graph:

|

| Graph #15 |

Looking at the bar graph, I now see that the 1953-1958 growth rate should have been higher. So I realize that the flat growth must have been part of the transition phase between growth and recession. I should have excluded it from the growth phase. Here's the revised graph, with the red line appropriately pruned back:

|

| Graph #16 |

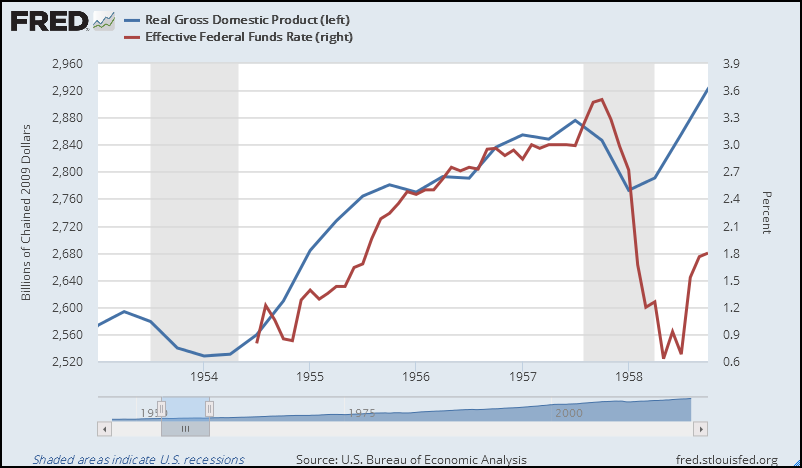

Here is RGDP (blue) for the same period (1953-1958) from FRED, along with the Federal Funds interest rate:

|

| Graph #17 |

Here is the bar graph, revised to show higher growth in the 1953-1958 period:

|

| Graph #18 |

The 1980-1982 value remains high, because I didn't change it. I don't know what would have happened if the Fed hadn't created the 1982 recession. (Well I do know: Growth would have tapered off gradually. The growth phase would have been longer, and the growth rate lower. But how much lower, I cannot say. I can only guess that it would fit the trend of decline visible in the other data on this bar graph.)

I won't revise the graph based on a guess. Nor will I consider the high value of the 1980-82 growth phase to be valid. In other words, I won't consider 1980-82 at all. I'll just omit it.

Given that, then, and converting quarterly growth rates to annual rates, this is the result:

|

| Graph #19 |

Myself, I would argue that growth-phase growth rates are a more telling indicator of economic health than business cycle growth rates. The growth-phase growth rate is growth at its best in each business cycle.

Coming out of recession, interest rates are low. Demand awaits fulfillment. And productivity is typically high, coming out of recession. These are features of the growth phase. So it provides a pretty good measure of the economy's "potential" (though that word has already been taken). Growth-phase growth shows our economy's performance is declining, and has been for a long time.

I bet you didn't see that coming.

Files:

RGDP & USREC (quarterly).xls (contains VBA code)

RGDP & USREC error checking & revisions.xls (contains VBA code)

Growth Phase Growth Rates.xls

10 comments:

ps: The VBA code is NOT fancy. I didn't even use range names in the code. I actually wrote cell and cell range addresses into the code, an embarrassingly bad practice. It works, but it ain't pretty.

"Growth definitely slowed when the interest rate went up. Growth slowed because the interest rate went up."

I can't understand how you can look at that graph and make such a statement. It seems pretty obvious to me that Fed interest rates are lagging behind GDP which suggests the correct conclusion is that the economy is driving Fed interest rates.

Richard Werner explains:

https://www.youtube.com/watch?v=6pU3tw5let4

Interesting link, all 26.33 of it.

"... the correct conclusion is that the economy is driving Fed interest rates."

You make it sound as if the whole of monetary policy is a hoax. That's a little hard to accept.

If I listened right, Richard Werner says credit growth drives economic growth. Okay, Steve Keen says the same thing, and many other people, and me. But it seems Werner wants to just jump in and start expanding credit, with no regard for the accumulation of debt and no regard for the cost of that accumulation. Maybe that's because of the questions that were asked, but something is definitely lacking in that discussion.

Thanks for the link. Maybe I'll listen to it again.

“Importantly for our disaggregated quantity equation, credit creation can be disaggregated, as we can obtain and analyse information about who obtains loans and what use they are put to. Sectoral loan data provide us with information about the direction of purchasing power - something deposit aggregates cannot tell us. By institutional analysis and the use of such disaggregated credit data it can be determined, at least approximately, what share of purchasing power is primarily spent on ‘real’ transactions that are part of GDP and which part is primarily used for financial transactions. Further, transactions contributing to GDP can be divided into ‘productive’ ones that have a lower risk, as they generate income streams to service them (they can thus be referred to as sustainable or productive), and those that do not increase productivity or the stock of goods and services. Data availability is dependent on central bank publication of such data. The identification of transactions that are part of GDP and those that are not is more straight-forward, simply following the NIA rules.”

http://eprints.soton.ac.uk/339271/1/Werner_IRFA_QTC_2012.pdf

Thanks Postkey. I did some searching myself and found a PDF where Werner takes the standard equation of exchange and compares it to the Irving Fisher version and explains the difference simply and well: The standard version excludes financial transactions. Wow.

The link has your name in it, by the way:

https://www.postkeynesian.net/downloads/Werner/RW301012PPT.pdf

Hello,

This is his latest interview.

“For many years, we’ve been told that finance is good and more finance is better. But it doesn’t seem everyone in the UK is sharing the benefits. On this program, we ask a very simple question – can a country suffer from a finance curse?

Host Ross Ashcroft is joined by City veteran David Buik and the man who coined the term Quantitative Easing, International Banking and Finance Professor Richard Werner.”

https://www.rt.com/shows/renegade-inc/379579-uk-finance-curse-suffer/#.WL23u0Kzmeg.twitter

"You make it sound as if the whole of monetary policy is a hoax."

A hoax by whom?

When I listen to Fed statements I hear them mostly saying they are reacting to economic conditions. I don't think what the Fed is doing is a hoax, but what some others say the Fed is doing is definitely a hoax.

The big problem I have with Werner is he acts as if all debt is bank loans. Bank loans are only 13% of total US debt. If it was closer to 100% Werner's theories would probably be valid. But you can't just pretend the world is something it isn't.

"The big problem I have with Werner is he acts as if all debt is bank loans."

I don't think so. It is the creation of net new money by the banking sector that 'drives' the economy?

Here is Werner:

"This explains why banks are special: They are not (just) financial intermediaries. They have a license to ‘print money’ by creating credit. There is no such thing as a ‘bank loan’. Banks do not lend money, they create money."

This isn't really accurate. At least not at all times.

During the housing bubble private investors financed more than $10 trillion in US mortgages through Mortgage Backed Securities. In other words, no deposits were created by these loans but securities were created instead.

In 2006 those securities were regarded to be as good as cash. They were universally being used for cash transactions. Even by mid 2008 the securities were still being called "money good" and were usually

accepted as money, but by the end or 2008 nobody would accept them as

money. What this means is that in a very short amount of time a huge

chunk of money disappeared from the economy. The chunk of money that evaporated was larger than the chunk of money that banks had created (bank deposits) by making bank loans.

To paraphrase Minsky anybody can create money - getting others to accept it as money is the trick.

Commercial banks really aren't special in terms of the ability to create money. They are special in times of crises when other forms of money are not being accepted. And that is probably the Fed's only real job - to make sure that the chunk of money that bank's create doesn't disappear in times of crises. The Great Depression was so bad because the Fed failed to do its job.

Thanks for that.

Post a Comment