UPDATE 5/4/2011 --

Gene Hayward has recently convinced me there is a problem in my breakout of public and private debt. I have to look at the numbers again, enough to get it right. Meanwhile, I am scratching out phrases like "only one-sixth the size" when I come across them.

Remember how it was after the towers fell?

Immediately, it seemed, everyone recognized the world was different. For years, it seemed, people spoke of pre-9-eleven and post-9-eleven. Still do. That day -- that moment -- was a turning point.

The financial crisis of 2008 was a comparable turning point; bigger, I think. For me, the "moment" was Treasury Secretary Henry Paulson's

speech of 19 September 2008.

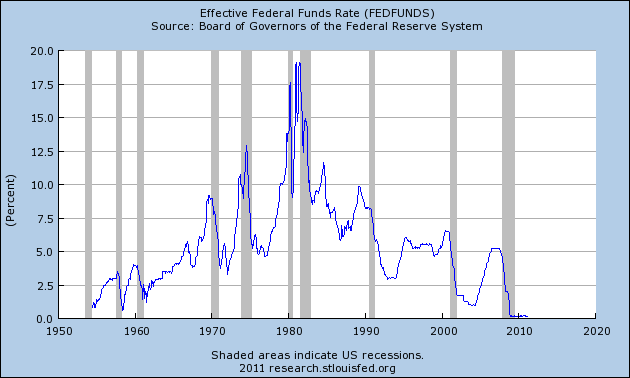

To put the moment in context, check out Bill Luby's graph in

Another Friday of Testing VIX Lows?. It shows a huge run-up in the Volatility Index against a background that shows a huge drop -- at the same moment, September '08 -- in the Dow (I think).

"From July 2007 to September 2008," Luby writes, "volatility was elevated, but seemingly contained." September '08 was the volatile moment, the moment of crisis.

An old post from January, 2008: Ron Robins'

Is the Amazing US Debt Productivity Decline Coming to a Bad End? Robins writes:

For decades, each dollar of new debt has created increasingly less and less national income and economic activity. With this ‘debt productivity decline,’ ...

Now, see, I like that: "debt productivity." It's wrong, of course. Debt cannot be productive. Credit-use can be productive. Debt is only the record of credit-use. But let's be flexible and go with common usage, for now.

The "productivity of debt" has been in decline for decades, Robins says. Agreed. It is an extremely important point, far more important, anyway, than media-people seem to think. I want to come back to this topic.

But first, let Ron Robins finish his thought:

...With this ‘debt productivity decline,’ new evidence suggests we could be near the end-game in this economic cycle. American collective consciousness will need to change to accept the new reality.

Yeah, I don't know about any "end-game" or what Robins may mean by that. And I don't know which cycle he's thinking of; the long-wave, I would guess, the one that ends in Great Depressions.

So then the end-game would be the depression.

I also don't know about "collective consciousness." Consciousness is a concept, like "moral argument," that is difficult for me to grasp. Kinda like the difficulty other people have to distinguish between "debt" and "credit."

Anyway, Robins. He says, "Getting less and less economic benefit from each dollar of new debt is becoming an enormous and onerous problem for the US." That's the

debt productivity thing. Robins quotes Grandfather Hodges:

“In 1957 there was $1.86 in debt for each dollar of net national income, but in 2006 there was $4.60 of debt for each dollar of national income – up 147%. It also means this extra $2.74 of debt per dollar of national income produced zilch extra national income. In 2006 alone it took $6.32 of new debt to produce one dollar of national income.” (Underlining added.)

"According to Dr. Kurt Richebacher..." Robins writes, "in 2005 ... [there was] $4.43 in new debt for each dollar of GDP growth. In 2006 ... it took $5.68 of new debt for each dollar increase in GDP."

The exact numbers differ, depending who reports them. But the numbers are close, and big, and increasing. On that, there is resounding agreement.

Yeah. Declining

credit efficiency or, as Robins calls it, declining "debt productivity." Some people may relate that concept to the observation that federal deficit spending

doesn't do much to stimulate the economy.

Eh. Yes and no. The decline in debt productivity affects government debt as well as private debt. And though government

policy is responsible for this whole mess, that is not to say it is government

debt that is responsible.

President Obama's large increases in federal deficits didn't happen until

after the crisis, so clearly they didn't

cause it. And if we look at accumulated debt,

federal debt total combined debt of U.S. federal, state, and local government is small potatoes compared to total private-sector debt,

only one-sixth the size.

Moreover, total government debt was

roughly stable in the U.S. from 1960 to 2008, relative to GDP, while total private-sector debt did nothing but increase. So lets jump away from any conclusions about government debt being the cause of the problem, and maintain for now a focus on total debt.

Ron Robins focuses on total debt. He has a good feel for the problem. But in my view he has no understanding of the cause, and no understanding of the solution.

Americans have gotten to this point as they sought fulfillment almost exclusively in the material world around them.

Robins blames... character, I guess. Another word I don't rely on. There is some kind of pathetic irony in blaming people rather than policy for the economic environment we're in. Some holier-than-thou superiority that interferes with reasoned discussion, and supersedes evidence.

The problem is not bad character. The problem is bad policy.

It is possible that the US Federal Reserve and the financial system will continue to produce ever increasing amounts of debt relative to national income and GDP...

Well Robins is right about this. In fact, I'd say that

continuing to produce ever-increasing amounts of debt is the only plan that makes sense to Ben Bernanke and other policymakers. Curse the luck.

In the years ahead many Americans will need to look more within themselves, rather than to material goods, to find personal fulfillment.

Yeah, the character thing again. The problem is debt, Ron. And the cause of the debt problem is policy. You know: "We need credit for growth." That policy. And: "Since growth is so hard to obtain, we need even more credit for growth." That.

Stop, Ron. Take a step back. Look at the insanity in those policies. They create debt.

The policies

create the problem.

Robins does not answer the question

why we are "getting less and less economic benefit from each dollar of new debt." He does not even

ask this question.

It is the total accumulation of debt that makes new debt less productive.

Existing debt

creates a drag on the economy. New additions to debt don't boost the economy unless they are more than big enough to offset the drag created by existing debt. And every new addition to debt creates more drag, making the problem worse.

We use credit for growth, but credit-use creates debt, and debt

hinders growth. So we use credit, and we grow, and we let debt accumulate, and we repeat the process until the accumulation kills off the golden

goose age.

And then we need a President like Reagan, bold enough to vastly increase federal deficits, to generate enough new credit-use to compensate for accumulated debt. But that solution is unsustainable, for it makes the accumulation bigger. Today, as a result of past policy, even Obama-size deficits cannot offset the accumulated debt.

It becomes a pointless exercise.

As long as people think we need to use more credit and accumulate more debt to make the economy grow, our policies are bound to fail. The more debt accumulates, the more it contributes to credit inefficiency and debt productivity decline.

{kind=link}