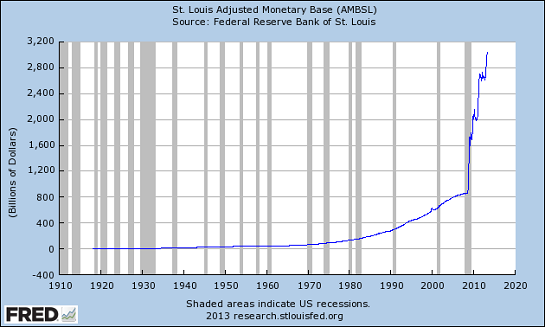

Somebody posted this graph at Reddit, along with a question:

Graph of US monetary base. Notice anything unusual?

|

| Graph #1: The Monetary Base |

In response to the graph, a number of your typical lowbrow comments:

Get ready for the coming category 5 inflationary stormand

Get prepared and wait the storm out over at /r/Silverbugsand

Brace yourself, inflation is comming.

Only one "m" in "coming", please. Anyway, here's a better question:

What was going on before that sudden final spike?

Questions like this might lead to better answers. We can look at the Graph #1 data a different way to get a hint of the better answers. Graph #2 shows "% Chg. from Yr. Ago" for the numbers from Graph #1:

|

| Graph #2: Percent Change from Year Ago of the Monetary Base |

Ah, this is much more interesting than the first graph. You can still see the big spike on the right, just before 2010. But there's lots of other stuff happening, too.

There are those three good-size spikes in the 1930s and '40s. That was a response to the Great Depression. That was Ben Bernanke's model for the big spike of 2008.

Notice that Bernanke's spike is much taller, and brief. Bernanke understood that it took a lot of increase in the monetary base to recover from the Great Depression, so he tried to do it all at once and get it over with. That's how it looks to me. If it didn't work, it's because there are other things involved than just the monetary base. And, granted, we still have problems. But I would say that the vertical gray bar that ends at 2010 is much narrower than the vertical gray bar that starts at 1930, because of the massive and rapid spike in base money. If nothing else, it drew people's attention away from economic collapse and focused that attention on inflation -- as you can see from the Redditors' remarks.

I don't mean to make excuses for Bernanke. His plan seems to be to keep trying "quantitative easing" until it fails spectacularly.

By the way, in mine of 4 June I related the Depression-era increase of the monetary base to inflation. I made reference to "three massive spikes" of inflation in that era. You can see those three spikes, in red, on the graph below. Each spike occurs approximately eight years after the corresponding spike in the monetary base:

.png) |

| Graph #3: The Rate of Money Growth (blue) and the Rate of Inflation (red) 1925-1970 |

Eight years is a long time, certainly longer than I would have thought. But the economy was unresponsive in that era, and this could account for the eight-year delay.

There is a fourth blue spike on the graph, just a hump really, between 1950 and 1955. Perhaps it is related to the Korean War? Anyway, about five years later there is a red hump of roughly equal size. This time there is only about a five-year delay between the monetary inflation and the price inflation.

Why five years instead of eight? Perhaps because the economy was more responsive... because the economy was growing again.

Finally, beginning around 1960 there is another increase in the blue, the monetary base. And sure enough five years later there is an increase, a comparable increase in the red, in the rate of inflation.

I never looked at this before. The relation is remarkable. I suppose I should point out that the relation seems to break down by 1970. The red inflation spikes of 1975 and 1980 on the next graph are higher than the growth of money, and less regular. And then after 1980 it's different again, and inflation runs significantly lower than money growth:

.png) |

| Graph #4: The Rate of Money Growth (blue) and the Rate of Inflation (red) 1950-1995 |

The reason the inflation spikes are higher in the 1970s? Others say "expectations". I say it was cost-push forces arising from the growth of finance. And the reason inflation ran low after the early 1980s? Changes in policy.

Unfortunately, those changes in policy caused growth to moderate, dropped interest rates to unnatural lows, and drove us to the Great Recession like lemmings to the sea.

What was going on before that sudden final spike?

There was a lot going on before 2008, before the base money spiked up. Look at the decade just before that massive spike. The years from 2000 to 2008 show a regular and persistent downtrend in the rate of money growth. When it reached zero, we got the Great Recession. Here, look again at Graph #2 -- between 2000 and 2010:

|

| Graph #2: Percent Change from Year Ago of the Monetary Base |

Now that's a pretty remarkable lower bound.

What else was going on, that we can see on Graph #2? Look at the rate of money growth before the increase of the 1960s. After the three Depression-era spikes, and before 1960. The rate of money growth in those years was very close to zero. The period even includes the fourth spike, the hump between 1950 and 1955 that we looked at above. That hump is only about half as high as money growth in the 1970s and '80s and '90s. Half as high, and of brief duration. Short, and close to zero.

So with all of this "close to zero" money growth going on in the 1950s, how come we didn't have another Great Depression or another Great Recession, then? I mean, in the 1920s and again in 2008 money growth only had to touch zero to bring the economy down. Why not also in the 1950s?

For one thing there was still plenty of money in the economy, left over from the three Depression-era spikes. When people already have plenty of money, you don't have to keep printing more money just so people can get hold of some.

But the big thing, I think, is that there was very little debt in the economy in the 1950s. Very little private debt. People were not burdened by debt. Repayment of debt was not a massive drain on the money that people had. We didn't need a lot of money growth to compensate for that drain, because that drain did not exist.

Oh, sure, there was a lot of debt in the economy in the 1950s if you look at government debt. We had lots of debt left over from fighting a world war. But that particular debt was evidently not a problem requiring a more rapid increase in money growth. The money growth could stay close to zero, even with a high level of government debt, because private debt was low.

But the economy was growing, and private debt was starting to accumulate.

What was going on before that sudden final spike?

What was going on, in the years before that sudden final spike, was the growth of debt. Mostly private debt, in fact.

|

| Graph #5: Total Credit Market Debt (blue), the Federal Share of it (red) and Base Money (green) |

See the zero line? Horizontal, faint gray, mostly hidden by the green line. All the area from the red line down to the zero line is debt of the Federal government. All the area from the red line up to the blue line is everybody else's debt, not the Federal debt.

What was going on in the years before 2008 was the growth of private debt.

Oh, and the green line? That's the monetary base. That's the money shown as the blue line on Graph #1. It shows the money the Federal Reserve put into the economy.

The green line shows how much money the Federal Reserve put into the economy. The red line shows how much the Federal government put into the economy. And from the red line up to the blue line shows how much debt the rest of us put into the economy.

But here's the thing: All of that debt, the red and the blue, is made up of multiple instances of the money shown as the green line. Multiple instances? Yeah, like in AutoCAD after you define a block you can insert it many times, but there is still only one block defined. Or like in object-oriented programming after you create an object, you can use multiple instances of it, but you've still created only one object.

Yeah, money is usually created from nothing. But when it's time to pay it back, you can't pay it back from nothing. To pay it back you need money in hand, or in your pocket, or in your wallet, or your bank account, or somewhere. The dollars we have to pay back are all instances of a money object. And each money object has to cover many instances, or there'll be hell to pay.

All of the money above the green line -- the money recycled by borrowing (red) and the money created by borrowing (blue) -- everything above the green line is money that costs interest.

+per+AMBSL.png) |

| Graph #6: Total Credit Market Debt and the Federal Share, per Dollar of Base Money |

Graph #6 shows the same three number sets as Graph #5, except this time each one is divided by base money. So the green line (base money) for example shows how many dollars of base money there are for each dollar of base money. Of course, there is just one dollar of base money for each dollar of base money, so the green line is now a perfectly flat and straight line with a constant value of 1.

The red line shows how much Federal debt there is, for each dollar of base money. Just by eye, it looks to be mostly between $6 and $8 dollars of Federal debt per dollar of base. So now, if every dollar of government debt carries an interest cost of 3%, the Federal government will be paying between 18 and 24 cents interest, per dollar of base money.

The blue line shows how much credit market debt there is in total, for each dollar of base money. At the high end, it ranged from $40 in 1994 to $60 in 2008. If every dollar of credit market debt carried an interest cost of 3%, the total interest cost in 1994 would have been $1.20 per dollar of base money, and in 2008, $1.80 per dollar of base money.

When debt accumulates to a high multiple of base money, the interest on that debt absorbs much or all of the base, leaving little or no money for anything else. In such conditions the Federal Reserve is forced to increase the growth rate of base money to maintain some measure of balance. Reduce money growth to zero in those conditions, and you create a Depression.

The sudden spike of base money shown on Graph #1 and fretted at Reddit is an attempt by the Federal Reserve to correct an imbalance. The upspike on Graph #1 is matched by the sheer drop of the blue line on Graph #6, as the Fed radically increased base money in an attempt to lower the level of that blue line.

Was it the right policy? No. The problem is not that there was too little base money. The problem was that there was too little base money relative to accumulated public and private debt. (Or possibly, relative to private debt, or to debt other than Federal debt, or something in that ballpark.) The problem is that there is too much debt.

And the correct solution in any case would have been to reduce accumulated debt.

What is it that creates the need for base money to spike up?

I took annual FRED data for total debt (1950-2012) and for base money (1918-2012) and put it in a spreadsheet with total debt numbers (1916-1970) from the Historical Statistics (Bicentennial Edition). The two debt series don't match up perfectly, but trends are trends and it is what it is:

| Graph #7: Debt Relative to Base Money, 1918-2012 The Google Drive Spreadsheet is available |

Notice anything unusual?

Total debt increased relative to base money until it created the Great Depression. Then there was a period of "correction", and a war. And then total debt increased relative to base money until it created the Great Recession.

Here's a question: What happens, that creates the need for base money to spike up suddenly in massive quantity?

Here's the answer: Debt accumulates until it creates problems. And then debt continues to accumulate, until some policymaker decides to do something about it.

3 comments:

Lots to chew on here.

I still think there is another dimension to this - the productivity of debt. You showed something significant about that the other day with this graph.

http://4.bp.blogspot.com/-WYE8wcfEKYE/UaxbZRI8MuI/AAAAAAAAIl8/2sM5g3HVBHo/s1600/TCU+per+TOTCI.png

If debt isn't going to support something useful - frex, capacity utilization - then what is it supporting? I say 1) speculation - mainly financial tail chasing in a derivatives market many times larger than total global GDP - and 2) rent gathering.

Both lead to further wealth accumulation, and neither of these is productive.

That's why the rich are getting richer and the economy cannot recover. There's a fork in the road ahead. One branch leads to the new dark ages [that, I think is the plan] and the other to blood in the streets.

I hope we choose wisely.

WASF!

JzB

I forgot to mention that immediately before reading this post, I read Krugman's from today, and he said this:

"those of us hoping to summon the expectations imp want to do so with policies that are at worst harmless, such as expanding the monetary base under conditions where this has no direct inflationary impact."

Contra the Reddit fools.

JzB

This is interesting.

http://slackwire.blogspot.com/2013/06/the-cash-and-i.html

Cheers!

JzB

Post a Comment