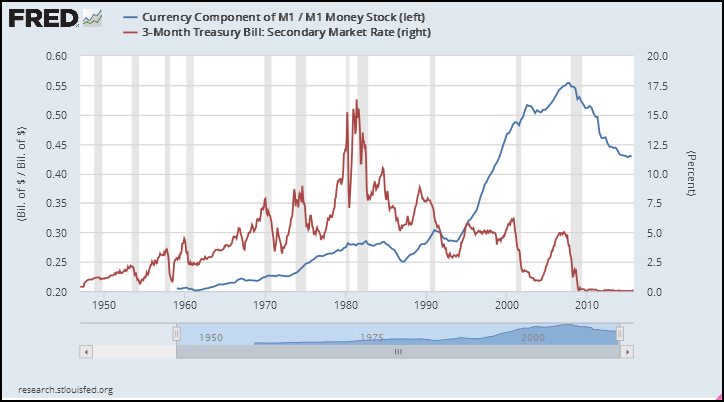

Scott Sumner:

Interest rates are the opportunity cost of holding cash. If you lower interest rates, people will choose to hold more cash. That means lower interest rates are contractionary. Here’s a graph showing the relationship between the demand for currency (as a share of GDP) and T-bill yields:

Notice that the two variables tend to move inversely.

Notice that the two variables tend to move inversely.

The graph is striking.

After a moment I figured it out: What's most striking is that graphs of economic data never look like that. They are never so obvious. Economic forces are always at odds with each other, and the graphs always show the tussle. Therefore, I don't trust Scott Sumner's graph.

Therefore, I don't trust his argument.

He shows his graph again -- with the blue line inverted -- and says

Those drops in cash velocity during the recessions (grey bands) are lower rates causing currency hoarding causing recessions.

"A causing B causing C." Nope. It's too neat and tidy. I don't trust it. There's gotta be a fishhook behind that worm.

Interest rates are the opportunity cost of holding cash. If you lower interest rates, people will choose to hold more cash.

Granted, that argument makes sense. But there are other facts about interest rates, and other causal inferences. You have to gather them all up and prioritize them. Prioritize them not according to how important they are to you, but how important they are to the economy. And then, remember that economic priorities change.

Then, and only then, is this muddy Sumnerism relevant:

Much of macro is balancing two seemingly incompatible ideas in your mind at the same time.

Scott Sumner didn't link to the FRED source page for his graph, so I had to recreate the thing from scratch:

|

| Graph #2: Currency Relative to GDP (blue) and the Interest Rate, à la Sumner |

That sounds to me very much like a description of GDP growth: A golden age after World War Two that peters out, perhaps by 1966, perhaps by 1974, and a definite slowdown of growth after 1980.

Sumner's blue line displays the inverted path of GDP, and not so much the path of the currency component.

I compared growth rates for GDP and currency. What's most obvious in that picture is inflation, which pushes both series up so that we see almost nothing below five percent from the early 1960s till 1990. Yikes.

Then I looked at those growth rates with inflation subtracted out, and the picture got interesting:

|

| Graph #3: A Comparison of GDP and Currency Growth Rates |

But try it this way: Before 1985, GDP growth runs high; after 1985, GDP growth runs low. See? It's not only that currency growth was greater when interest rates were falling. Currency growth was greater, and GDP growth was less.

If you take GDP and currency in billions, annual, and compare the 30-year periods of growth before and after 1981 -- Sumner's date -- it turns out that GDP growth slowed down more than currency growth speeded up.

Compare 25-year periods instead (to exclude the crisis) and it remains true that GDP growth slowed more than currency growth speeded up.

For Sumner's blue line, GDP is the dominant factor. Not currency.

But let me ask the question: Why is he looking at currency relative to GDP? Because it seems to support his argument?

Is GDP really the best choice for context? Or is that choice just routine, something you put in parentheses when you describe a graph?

Suppose we try something different. Suppose we don't look at the currency component of M1 money relative to GDP. Suppose we look at the currency component relative to all of M1 money instead. This allows us to see what happened to the money rather than what happened to GDP:

|

| Graph #4: Currency Relative to M1 Money (blue) and the Interest Rate |

The currency component was increasing as a share of M1 all the while, until the crisis. Sumner doesn't show it.

Sumner wants us to look at the portion of our spending-money that we choose to hold as cash. That is precisely what the "Currency Component of M1" is. But Sumner shows it relative to GDP. That's irrelevant and meaningless. The currency component of M1 is part of M1 money, spending-money.

My graph shows the spending-money that we choose to hold as cash, as a portion of all the spending-money that we have. Sumner's does not.

Sumner's graph is meaningless because of his choice of GDP as context for currency. It does give a nice, decorative line that looks like it supports his argument, even though it doesn't. His blue line is meaningless, because of his careless context.

Want to go again? Here is the currency component of M1 relative to a bigger, newer money measure, MZM:

|

| Graph #5: Currency Relative to MZM Money (blue) and the Interest Rate |

Within the limits noted -- limits which include the rise and fall of the interest rate -- within those limits, the only area where the blue does not cling to the red is from 1989 to 2007. Yet even for that period the blue line traces the same general path as the red. Sumner's graph shows nothing comparable.

And after its 1995 peak the blue races downward to meet the red. So it is only from 1989 to 1995 that the blue line appears to misbehave.

But you know what? That's pretty much the same period of time when M1 money showed unusual increase. You know the story: I tell it all the time. M1 showed unusually rapid increase. Accumulated debt showed unusually slow increase. Debt-per-Dollar showed an anomalous reduction. And then, like magic, the economy was good for a while.

I'm onto something. Sumner is not.

No comments:

Post a Comment