I corrected for inflation too soon. That has to be it. That's the only change I made to the numbers. All the other stuff was just getting the numbers, or showing them.

Couple days back I looked at Gross Federal Debt as a Percent of GDP. Looked for a trend. Found one.

Or invented one. Whatever.

Looked at that trend, long-term. And wanted to find the economic growth that would have kept the federal debt number going down, kept it following the trend.It's backwards from what everybody else does. Everybody else looks at Federal Debt Relative to GDP and says the federal debt is too high.

But the original complaint, remember, was that economic growth was too slow: GDP was not increasing fast enough. So to me, backward is the right way to go. Rather than focusing on squishing down the federal debt, I want to consider the growth we would have needed, to make the federal debt seem size-reasonable. Then I want to look at that growth and see if it is realistic.

Anyway, I'll make a new spreadsheet. And this time I'll correct for inflation later.

I'll keep the original sheet called TABLE, which has the source numbers untouched.

I'll keep my Sheet1, where I develop the numbers for the exponential trend.

And I'll keep my Sheet2, where I develop the Gross Hypothetical Product. But I'll delete from that sheet the GDP Deflator and the inflation-adjusted GHP. And I'll delete Sheet3 and Sheet4, where I used the inflation-adjusted numbers and my graphs went astray.

On Sheet2 I'm adding the column "Gross Federal Debt as a percent of GHP." That's redundant, because it'll give me the exponential trend numbers again. But at least I can do a graph, and I have numbers to use for GHP.

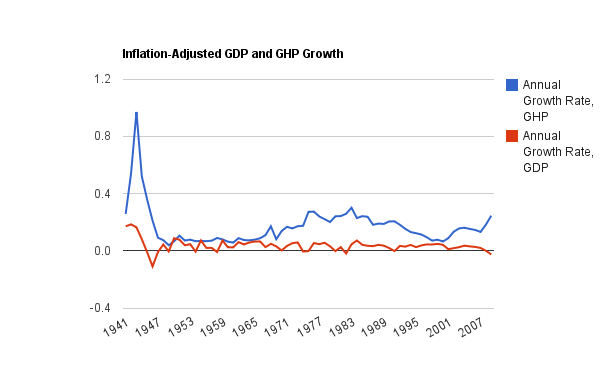

Let's compare GHP to GDP. No inflation-adjustment. The GDP numbers -- actual, or "nominal" this time -- again come from Measuringworth.

Wow. These numbers are big. The GHP makes the GDP look small. It doesn't look like "realistic" growth. What this means I guess is that debt really took off. And you can see some kinks in the red line, where it suddenly starts going up faster than it did before. That's driven entirely by the growth of federal debt.

That's not something you'd normally hear me say. But I have to say what the graph says. Still, it's much too early to draw any conclusions.

Let's cut off some of that right end of the graph, and look at it where the lines are closer. I'll stop this time at 1982:

There is a definite break with the trend. A closer close-up shows the break occurring between 1974 and 1975 or -- more accurately -- shows the change in 1975 and after:

"That is enough for today!"