I like to see what word origins tell me.

These two scans are from the yellowed pages of Webster's New Twentieth Century Dictionary of the English Language, unabridged; The World Publishing Company, Cleveland and New York, 1950.

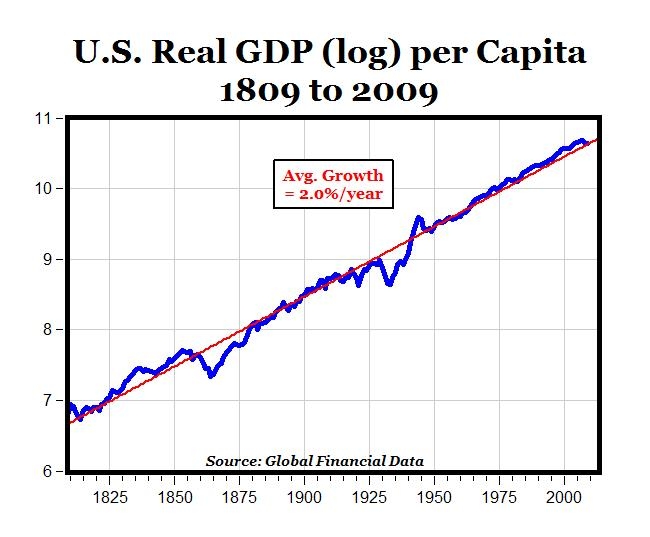

Now I have to say, I have never come across a Mark J. Perry post that I thought was any good at all. But I don't go looking for Perry garbage. I trip over it. As you know, I'm fascinated by graphs and by GDP growth. I left that link on my desktop a while back because it looked interesting.

Ha.

I tried to duplicate the graph. It's a joke. Perry says the growth works out to 2% per year. But it's only about 1.75%.

When it comes to long-term growth rates, 1.75% is not even close to 2%. After 200 years, 1.75% growth produces a 32-fold increase. 2.0% growth produces a 52-fold increase. There's no comparison.

It could be a rounding error -- but it can't be a rounding error, because they don't call it two percent. They call it two point oh percent. 2.0% means the number before rounding was between 1.95 and 2.049 or so. 1.75% would round to 1.8%, not 2.0%

So, it's bullshit.

|

| Graph #2: Real GDP per Capita (blue) and 2% Growth (red) (Not on a Log Scale) |

Neoclassical economics has since long given up on the real world and contents itself with proving things about thought up worlds. Empirical evidence only plays a minor role in economic theory, where models largely function as a substitute for empirical evidence.

About the first thing I noticed was that hardly any of the graphs in the textbook were based on actual numbers.

A rich country, in the same manner as a rich man, is supposed to be a country abounding in money; and to heap up gold and silver in any country is supposed to be the readiest way to enrich it. For some time after the discovery of America, the first inquiry of the Spaniards, when they arrived upon any unknown coast, used to be, if there was any gold or silver to be found in the neighbourhood? By the information which they received, they judged whether it was worth while to make a settlement there, or if the country was worth the conquering.

Plano Carpino, a monk sent ambassador from the king of France to one of the sons of the famous Gengis Khan, says, that the Tartars used frequently to ask him, if there was plenty of sheep and oxen in the kingdom of France? Their inquiry had the same object with that of the Spaniards. They wanted to know if the country was rich enough to be worth the conquering.

Among the Tartars, as among all other nations of shepherds, who are generally ignorant of the use of money, cattle are the instruments of commerce and the measures of value. Wealth, therefore, according to them, consisted in cattle, as, according to the Spaniards, it consisted in gold and silver. Of the two, the Tartar notion, perhaps, was the nearest to the truth.

As I argue in the paper, during the Great Inflation period of the 1970s, members of the FOMC regularly asserted that the process of inflation determination had changed. Relying on public statements and personal diary entries from Arthur Burns, I demonstrate that there is little evidence that the Federal Reserve was less concerned with inflation during the 1970s. Rather, the view of Burns and others was that inflation was largely a cost-push phenomenon. Burns thought that incomes policies were necessary to restore price stability and stated that “monetary and fiscal tools are inadequate for dealing with sources of price inflation that are plaguing us now.”

The shift in policy, beginning with Paul Volcker, was an explicit attempt to stabilize inflation expectations and this was done deliberately at first through monetary targeting and ultimately through the stabilization of nominal income growth. Gone were notions of cost-push versus demand-pull inflation.

Josh: “Rather, the view of Burns and others was that inflation was largely a cost-push phenomenon. Burns thought that incomes policies were necessary to restore price stability and stated that “monetary and fiscal tools are inadequate for dealing with sources of price inflation that are plaguing us now.””

People forget (and maybe younger people never knew) just how common that view was in the 1970′s. It was common among economists as well as the general population. It was almost the orthodoxy of the time, IIRC. Tighter monetary policy would just raise interest rates, which would increase costs, and make inflation even worse.

Burns’ view is consistent with the orthodoxy of the time — as epitomized, for example, by Samuelson and Solow (1960).

There were really _economists_ who thought that “tighter money” would raise inflation through a cost-push mechanism?

And yet another factor has been the undue reliance on restrictive monetary policy to limit demand, with the perverse result of making interest rates themselves a major cost-push force.

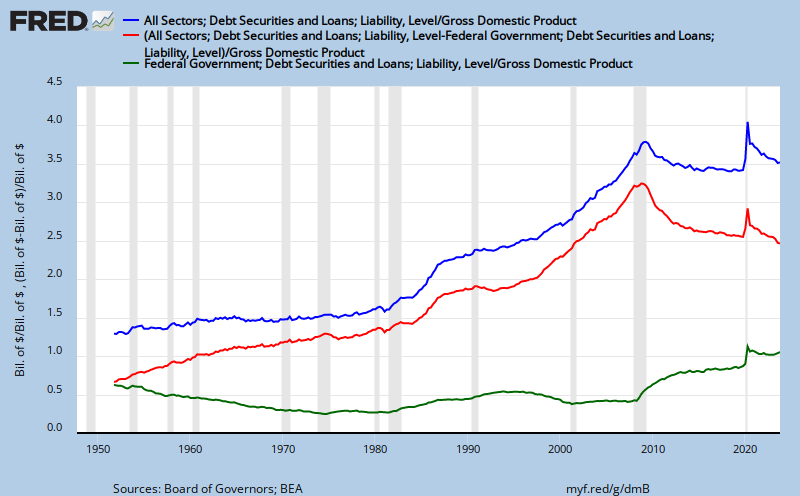

There is mounting evidence that at high private debt loads, the purchasing power of debt has diminishing returns... If so, it might be the case that small amounts of public debt at low private debt/GDP ratios can purchase staggering GDP growth rates, but that large amounts of public debt at high private debt/GDP ratios will purchase decreasingly positive GDP growth rates until the GDP growth rate is zero.

If so, it might be the case that small amounts of public debt at low private debt/GDP ratios can purchase staggering GDP growth rates, but that large amounts of public debt at high private debt/GDP ratios will purchase decreasingly positive GDP growth rates until the GDP growth rate is zero.

In reality high profits tend much more to raise the price of work than high wages. If in the linen manufacture, for example, the wages of the different working people, the flax-dressers, the spinners, the weavers, etc., should, all of them, be advanced twopence a day; it would be necessary to heighten the price of a piece of linen only by a number of twopences equal to the number of people that had been employed about it, multiplied by the number of days during which they had been so employed. That part of the price of the commodity which resolved itself into wages would, through all the different stages of the manufacture, rise only in arithmetical proportion to this rise of wages.

But if the profits of all the different employers of those working people should be raised five per cent, that part of the price of the commodity which resolved itself into profit would, through all the different stages of the manufacture, rise in geometrical proportion to this rise of profit. The employer of the flaxdressers would in selling his flax require an additional five per cent upon the whole value of the materials and wages which he advanced to his workmen. The employer of the spinners would require an additional five per cent both upon the advanced price of the flax and upon the wages of the spinners. And the employer of the weavers would require a like five per cent both upon the advanced price of the linen yarn and upon the wages of the weavers.

In raising the price of commodities the rise of wages operates in the same manner as simple interest does in the accumulation of debt. The rise of profit operates like compound interest.

If you’re not convinced that today’s consumers are better off than at any time in history, spend some time browsing the old Sears, Wards, and J.C. Penney’s Christmas catalogs...

In my course I have basically been taught that the free market is the most efficient and best system in the world and trouble always results when it is interfered with. In my textbooks recessions are not mentioned, they do not happen. There is no explanation of unemployment, the biggest issue of our times. There is no mention of profit, the heart of capitalism. Nor do they talk about banks or money or advertising or how systems are guided by power relations. No mention is made of poverty, in effect ignoring three-quarters of the world.

The idea that the market could fail is never given a moment’s thought. The market is always assumed to be in equilibrium, providing the greatest good for the greatest number of people. If you thought the current crisis would have changed this thinking then you would be wrong. The older pre-recession editions of textbooks are essentially the same as the newer post-recession textbooks. Mainstream economics has cut itself off from the real world and instead built a fantasy utopia.

Unemployment is a thought never far from mine or my generations mind. It is the biggest problem affecting millions of people the world over, yet traditional economics offers no explanation of it. I will graduate with a degree in economics in six months time, yet I couldn’t tell you why some people are unemployed.

Yesterday I noted that the preoccupation with the size of the current deficit — which, as everyone reminds us, is ONE TRILLION DOLLARS — is completely misguided. Since then I’ve done some more arithmetic, which solidifies the point.

So, in fiscal 2012 (which ended September 30) we did in fact have a federal deficit of $1.1 trillion (pdf). The question is, however, whether this deficit represents, as everyone claims, a fundamental mismatch between what we want and what we’re willing to pay for — or whether it’s mainly just a reflection of the depressed state of the economy.

we don’t need a balanced budget to have a stable fiscal situation; all we need is for debt to grow no faster than GDP.

OK, revenues were $2.45 trillion, which was 15.7 percent of GDP, at $15.5 trillion. The CBO estimates, however, that potential GDP — what the economy would have produced at full employment — was $16.5 trillion over the same period. And if the economy had been at more or less full employment, we wouldn’t just have collected taxes on the additional income; historically, the tax share of GDP varies strongly with the business cycle. If the economy had been at potential and revenue had been a historically normal 18 percent of GDP, revenue would have been more than $500 billion more than it was; even if revenue had been only 17.5 percent, it would have been almost $450 billion more than it was.

The question is, however, whether this deficit represents, as everyone claims, a fundamental mismatch between what we want and what we’re willing to pay for — or whether it’s mainly just a reflection of the depressed state of the economy.

|

| Graph #1: Money in the Spending Stream per Dollar's Worth of Output Click Graph for FRED Source Page |

|

| Graph #2: Total Credit Market Debt Owed per Dollar in the Spending Stream Click Graph for FRED Source Page |

the lack of confidence businesses and individuals have in Washington’s ability to ensure stable market conditions.

Unlike in the run-up to the 2008 crash, when businesses took too much risk, today they are not willing to take risks we need them to take.

The steps we need Congress to take to get the economy moving again do not require money; they require leadership.

| Graph #1: Debt at the Peak |

The farmer, compared with the proprietor, is as a merchant who trades with borrowed money compared with one who trades with his own. The stock of both may improve, but that of the one, with only equal good conduct, must always improve more slowly than that of the other, on account of the large share of the profits which is consumed by the interest of the loan.

The primary difference between today and the 1930s, when the U.S. experienced its last systemic crisis, has been the response by policymakers. Having the benefit of hindsight, policymakers acted swiftly to avoid the mistakes of the Great Depression by applying Keynesian solutions.

|

| Graph #1: RGDP Fitted to the Trend Lines |

|

| Graph #2: Stages of the slowdown in real growth |

|

| Marcus's graph |

It´s more or less recognized that US RGDP is trend stationary (maybe that´s changed now!), with real growth averaging about 3.3% from the early 50s to 2007

|

| Graph #1: Discontinued (blue) and New (red) Fed Holdings of Federal Debt, Relative to GDP |

|

| Graph #2: Discontinued (blue) and New (red) Fed Holdings of Federal Debt, Relative to TCMDO |

I remained the whole day in seclusion, with full opportunity to occupy my attention with my own thoughts. Of these one of the very first that occurred to me was, that there is seldom so much perfection in works composed of many separate parts, upon which different hands had been employed, as in those completed by a single master.

Thus it is observable that the buildings which a single architect has planned and executed, are generally more elegant and commodious than those which several have attempted to improve, by making old walls serve for purposes for which they were not originally built.

"Let's begin with the premise that everything you've done up to now is wrong."

we have to radically change the way we conceive of and model the economy.

The simple question that was raised during a recent conference organised by Diane Coyle at the Bank of England was to what extent has - or should - the teaching of economics be modified in the light of the current economic crisis? The simple answer is that the economics profession is unlikely to change.

Does this mean that we should cease to teach ‘standard’ economic theory to our students? Surely not.

|

| GREEN: The Federal debt RED: Everybody else's debt BLUE: Total Credit Market Debt Owed |

|

| Graph #1: The Gross Federal Debt, and Federal Debt not held by the Federal Government. Click graph for FRED source page. |

|

| Table #1: Compound Annual Growth Rates |

For every debtor there is creditor, thus if debtors cut back on spending to deleverage then creditors should be receiving more funds with which they could provide an offset in spending.

The architects of Reaganomics styled themselves Supply-Siders. They scorned the Demand-Side theories and policies they attributed to John Maynard Keynes and to his "liberal" followers...

...employers would make a loss if the whole of the increased employment were to be devoted to satisfying the increased demand for immediate consumption. Thus, to justify any given amount of employment there must be an amount of current investment sufficient to absorb the excess of total output over what the community chooses to consume...

The proportion of the disposable income which individuals desire to spend on consumption is known as propensity to consume. MPC is the proportion of additional income that an individual desires to consume.

|

| Graph #1: Consumption Spending goes up Less than DisposableIncome. |

|

| Graph #2: Personal Saving as a percentage of Disposable Personal Income |