Yesterday we reviewed Clonal's thoughts on inequality and debt:

1. For the 90%, real wages stagnated.

2. Their debt load increased.

3. The interest on this increased debt load went to the top 1%.

4. Debt drives inequality

I like it because it is short and easy to grasp. And I like it because Clonal says it's debt that drives the inequality, not the other way around.

Okay. It's both ways, to be sure. People getting shorted by income inequality find themselves borrowing when they'd rather not. Their inequality drives their debt. Sure. That happens, too.

Today I reconsider Steve Waldman's Inequality and demand from a year ago. Steve's thoughts are similar to Clonal's, but Steve presents a longer, more fully developed argument.

1. For the 90%, real wages stagnated.

"Let’s start with the obvious," Waldman writes. " ... In the US we’ve seen inequality accelerate since the 1980s, and until 2007 we had robust demand [and] decent growth ..."

(I think robust and decent is an exaggeration, but hey.)

He points out that "the rich do in fact save more" than the rest of us. "So how," he asks, "do we reconcile the high savings rates of the rich with the US experience of both rising inequality and strong demand over the 'Great Moderation'?"

In other words: If income increasingly accrues to the rich, who spend little of it, what accounts for the strong demand during the Great Moderation? Where did the money come from, that people were spending?

2. Their debt load increased.

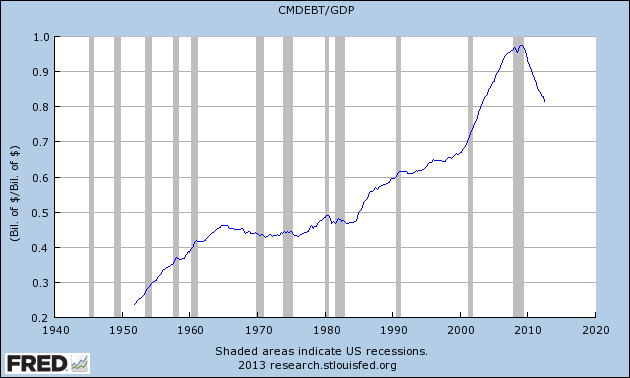

It came from the growth of debt, Waldman says: "Sure enough, we find that beginning in the early 1980s, household borrowing began a secular rise that continued until the financial crisis." He shows household debt relative to GDP:

|

| Graph #1: Steve Waldman's FRED Graph of Household Debt relative to GDP |

He says the graph "shows household borrowing as a fraction of GDP". Actually, it shows household debt as a fraction of GDP. Debt is the accumulation of borrowings.

It's tempting to think that each year's increase on the graph is due to "borrowing". But that's not the whole story, as JW Mason points out. "Changes in debt-income ratios reflect a number of macroeconomic variables," Mason says. But I made that point six months back, and I don't mean to harp on it now.

It's a good story, Steve Waldman's story: We used more credit because our income was falling behind. Turbocharged by credit, our spending created Waldman's "robust" and "decent" economy, but our debt accumulated. It was unsustainable.

3. The interest on this increased debt load went to the top 1%.

At this point, Clonal's story and Steve Waldman's go in different directions. Clonal points out that the increasing cost of that debt translated into increasing income for savers -- for the rich, then, because "the rich do in fact save more" than the rest of us. Clonal sees interest cost and interest income as the vehicle moving income from those with less income to those with more income. He sees debt as a driver of income inequality.

Steve Waldman looks at interest rates instead of interest costs. He points out "the slow and steady decline in real rates that began with but has outlived the 'Great Moderation'". He says

My explanation is that growing inequality required ever greater inducement of ever less solvent households to borrow in order to sustain adequate demand, and central banks delivered.

In other words, the Fed pushed interest rates down to get people to borrow more, to stimulate the economy and keep aggregate demand where they wanted it. Makes sense to me; that's what the Fed does. But in Steve's view it's inequality that drives the growth of debt -- just the opposite of Clonal's view.

I should say, there is no conflict between Steve Waldman's story and Clonal's. Both could be true. To my way of thinking, both are true.

But observe that in Waldman's story the inequality comes first. The increase in borrowing comes next, as a way to compensate for incomes failing to keep up. Falling interest rates are applied as needed, to induce increased borrowing. And all of this begins, according to Waldman, in the 1980s: "In the US we’ve seen inequality accelerate since the 1980s", he writes. And "beginning in the early 1980s, household borrowing began a secular rise".

That's where my problem lies.

Clonal sees debt as a problem because it drives inequality.

Steve Waldman sees household borrowing as a bad solution because it isn't sustainable under conditions of deepening income inequality.

I agree: Inequality is a problem because it drives debt, and because increasing income inequality isn't sustainable. Debt is a problem because it drives inequality, and because debt growth isn't sustainable.

But if household borrowing began its secular rise before the early 1980s -- before the acceleration of inequality since the 1980s -- and if debt is a problem, then maybe, just maybe, debt is the problem that initiated the rise of inequality.

What was it Clonal said? Debt drives inequality. If that's true, you don't have to have inequality to start with. You can create inequality just by accumulating too much debt.

The question, then, is whether it is correct to say that "beginning in the early 1980s, household borrowing began a secular rise". Let's look at a graph.

Graph #2 shows the same debt relative to the same GDP as Steve Waldman's graph shows. But #2 shows the change in that debt, the increase or decrease in billions of dollars. Not the gross accumulation of that debt. It's the change in debt that shows new borrowing. So: When did the secular rise in household borrowing begin?

|

| Graph #2: Change in Household debt (in Billions) as a Percent of Nominal GDP The red line is the Hodrick-Prescott trend line for the quarterly data (Lambda = 1600) |

The red line shows the trend of quarterly debt growth consistently below one percent of GDP until the early 1970s, and consistently above one percent of GDP from the early 1970s to the early 1990s.

There is no sudden, secular rise in household borrowing that begins in the early 1980s. There is only a large cyclical interruption of the rising rate of borrowing, due to the double-dip recession of the early 1980s.

There is no sudden, secular rise in borrowing that offsets the acceleration of inequality. If there was, then maybe economic growth would have been as good after 1980 as it was before.

So, okay. Robust and decent was an exaggeration. The economy wasn't so good after 1980 because of inequality and debt, and because new borrowing did not fully compensate for the acceleration of inequality. I buy all of that. It makes me shudder to think of the growth of debt as insufficient, but the story makes sense.

But the timing is wrong. The increase in borrowing did not begin in response to the rise of inequality. The growth of borrowing began first. It began in the early 1970s, or the early 1960s maybe, well before the acceleration of inequality.

So it is possible that the growth of borrowing, the growth of financial cost in the 1960s and 1970s was the problem that created the rise of inequality.

It's possible. But it's not that direct and simple, in my view. The growth of financial cost, like the growth of any cost, hindered the production of output and lowered profits. Meanwhile, the growth of financial income provided an appealing alternative to productive activity. Finance drew investment away from the productive side. But this only increased the growth of financial cost, further reducing profit.

Business responded by squeezing wages, which became the acceleration of inequality. Policymakers responded with supply-side economics, protecting and reinforcing the growth of inequality.

But the problem didn't begin with inequality in the 1980s. It began with the excessive borrowing, insufficient repayment, and the excessive accumulation of debt in the 1960s and '70s.

5 comments:

Saying that the rich save more has to be further peeled back I think. Obviously they make more so the number of dollars they can save is much more. I also think they save a greater percentage of their dollars because while their costs of living are higher I think they have a smaller percentage of their income going to their needs. Its also important to remember that they save differently as well. Many people outside the 10% simply save dollars in an account that earns interest, while the wealthy buy things which are savings vehicles and will appreciate. So I think many of the savings charts are actually looking at the present prices of things which have been bought to save in. As the stock market appreciates, they don't actually get more dollars in saving, but the price of what they save appreciates.

They live in a different world than the average guy and when they talk about their savings its not just dollars in an account or in a cookie jar like many in the lower rungs, its assets which fluctuate in prices and they have the fed on their side keeping those asset prices form falling too much.

Ultimately though they want to sell those assets and its the stockbrokers job to try and convince enough of us rubes to buy them from the rich guys.

Monetary policy is designed to make debt more affordable for the little guys. It doesn't give you more dollars it stretches your dollar by allowing you to lower present payments but make them for a little longer....... string you along

So the debt drives the inequality as clonal says

And this inequality isn't a cause its a result of policies

Something isn't adding up.

Look at simple CMDEBT growth, no denominator.

http://research.stlouisfed.org/fred2/graph/?g=qHG

Clearly, debt growth after 1980 is consistently greater than before.

In your graph 1, the Debt/GDP line is essentially flat from mid 60's to early 80's, and until the late 70's is consistently below the mid 60's value.

This makes sense with the graph I posted above, but not with your graph 2.

When I try to reproduce your graph 2, I get this:

http://research.stlouisfed.org/fred2/graph/?g=qHI

And then have to manually change the units on line B [GDP] from "Change, billions of dollars" to "Billions of dollars."

The FRED math is done behind a curtain. I'm guessing something blows up in their algorithm when you go through these steps.

If you want to get a rate of change for the graph 1 data, I think you have to go at it this way, which presents a much more complex picture.

http://research.stlouisfed.org/fred2/graph/?g=qHK

The value increases all through the 70's, but never goes above the low 60's high until well into the 80's.

Cheers!

JzB

"low 60's high" should be "early 60's high."

Jazz: "Look at simple CMDEBT growth, no denominator.

http://research.stlouisfed.org/fred2/graph/?g=qHG

Clearly, debt growth after 1980 is consistently greater than before."

Yeah, that's a good graph. Clearly, debt growth after 1975 is consistently greater than before.

Clearly, debt growth after 1970 is consistently greater than it was before.

Clearly, debt growth after 1960 is consistently greater than it was before.

//

Jazz: "When I try to reproduce your graph 2, I get this:

http://research.stlouisfed.org/fred2/graph/?g=qHI

And then have to manually change the units on line B [GDP] from 'Change, billions of dollars' to 'Billions of dollars.'

The FRED math is done behind a curtain. I'm guessing something blows up in their algorithm when you go through these steps."

You're guessing something blows up in their algorithm??

When you choose "Change, billions of dollars" units for line A -- CMDEBT -- FRED assumes you want to continue selecting those units for the next data you add to the graph (your line B). This is consistent FRED behavior, and has been for quite some time. I find this behavior quite irritating, actually. It makes it easy to get the wrong graph, as you did.

BTW you can get to the FRED Graph version of my Graph #2 by clicking the "FRED graph " link in the first paragraph after Graph #2. It shows the recessions that I talk about in that paragraph.

(Your inability to reproduce Graph #2 is not evidence that Graph #2 is incorrect.)

//

Jazz: "If you want to get a rate of change for the graph 1 data, I think you have to go at it this way, which presents a much more complex picture.

http://research.stlouisfed.org/fred2/graph/?g=qHK

The value increases all through the 70's..."

My point, exactly: "there is a definite increase in borrowing from the late 1960s to the early 1970s to the late 1970s -- all well before the acceleration of inequality and borrowing in the 1980s."

I just made a long and detailed response which evaporated into the ether when i tried to post it.

If I didn't already have a head ache, I'd get drunk.

Short version.

Clearly, debt growth after 1970 is consistently greater than it was before.

Clearly, debt growth after 1960 is consistently greater than it was before.

Detailed analysis [now lost] of the data shows these statements not to be correct.

For debt to contribute to inequality, it has to inhibit wealth accumulation. There is some threshold below which it doesn't.

But this will vary across income and prior wealth levels, so aggregated data might not give a true picture.

At the very least, I'm going to go chew nails.

JzB

Post a Comment