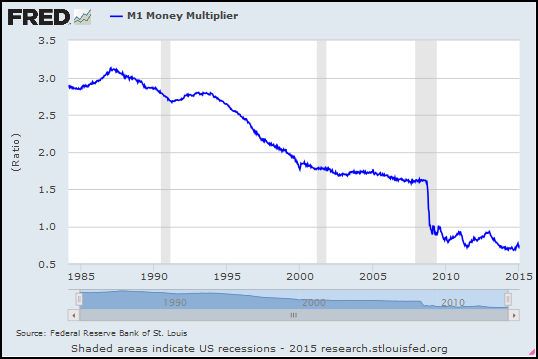

You can dismiss this graph because it shows something called the money multiplier,

|

| Graph #1: The Money Multiplier |

Here's what I might do: Put a line on the graph.

|

| Graph #2: The Red Line shows the Low Edge of a Trend Channel |

Midway between those two periods, the blue line runs very close to the red for a good four years, punching thru it just once, at the end of 1999.

It is as if something set a minimum, a downtrending boundary below which the money multiplier could not fall, except by waiting for the passage of time to push that boundary lower. An interesting notion. But there is more.

There are stories, there must be stories behind those disturbances where the blue line runs up and away from the red -- in the early 1990s, then again in the 2000s -- and returns to the red line, once gradually, once suddenly. There must be stories.

The sudden return to red in the midst of the 2009 recession, that's crisis-related. Bernanke-related. That's an obvious one. But how about the eight years before that sudden drop? That is almost the whole decade of the 2000s, and all that time the money multiplier was running nearly flat. There was a stiff resistance to downtrend in the multiplier at that time. Now that's interesting. And that was during the Bush years.

Explain?

That's the second of the two disturbances. The other, the first, begins just after the 1990 recession, peaks at the end of 1993, and returns to red by around mid-1997. Can you explain this one? I think I can.

The blue trend away from red -- from early 1991 to late 1993 -- matches up with a unique downtrend in the debt-per-dollar (DPD) ratio. And the blue return to red -- from late 1993 to mid-1997 and then further, to the end of 1999 -- matches up with the return-to-trend of the DPD.

I went back and started with the blue line again, the money multiplier from Graph #1. I added my debt-per-dollar ratio in green.

|

| Graph #3: The Money Multiplier (blue) and Total Debt per Dollar (green) |

Both of these ratios use FRED's M1SL data series. This may account for some of the similarity that will soon become apparent. The blue line divides M1SL by the monetary base AMBSL. The green line divides accumulated public and private debt, TCMDO, by M1SL.

Next I eyeballed two trend lines -- red for the money multiplier, and black for debt-per-dollar.

|

| Graph #4: The Multiplier and DPD with Trend Lines |

For the same 1990-2000 period, you can see a disturbance where the green line moves away from the black, and then gradually returns. These two disturbances, the blue and the green, occur at the same time and display similar shapes. Except the one is the mirror opposite of the other.

I took Graph #4 and highlighted the disturbance areas:

|

| Graph #5: The Multiplier and DPD with the Disturbances Highlighted |

What does it mean? I don't know. But I don't need to know what it means, today. I never looked at the money multiplier this way, before today. I don't want to jump to any conclusions.

We have the beginning years, the middle years, and the ending years of the money multiplier all fitting themselves to that down-trending red line. And we have explained the first disturbance, the disturbance of the 1990s. All that remains is the second disturbance, the Bush years disturbance. Oh, but you were going to explain that one.

But hey, it's the money multiplier we're looking at here, so maybe you should just dismiss it.

It's your choice.

5 comments:

I still think that if you're going to look at debt/dollar as a negative economic influence, you should back public debt out of the picture.

Maybe it should be honed down to consumer debt + mortgages.

The economy is about 70& driven by consumer spending. That's my rationale for saying this.

Re: your graph 4, the contrary motion we see between about '87 and '02 is specific to the period, and doesn't exist before or after.

This might be coincident correlation or just a data artifact.

it bothers me that it appears, then after a while, disappears.

Cheers!

JzB

I think it's useful to be very specific about what the money multiplier is, how it's conventionally used and what it means to dismiss it.

The money multiplier is just a ratio of two monetary aggregates, base and broad money. The way it's conventionally used is to tell a causal story about how a change in base produces a change in broad.

The dismissal is narrow and very specific to that causal story. It's not a blanket objection to taking those two or for that matter any two numbers, juxtaposing them in a ratio and trying to draw some insight from the results, maybe the footprint of something interesting, by all means... that's exactly the sort of thing I come here hoping to find.

With the requisite disclaimers taken care of, on to the interesting stuff which is the question you posed.

I don't have an answer but I do have the beginning of an inquiry. I start by decomposing the money multiplier into its component parts.

The first thing that jumps out at me is that base money is smooth until 2008. This is readily explained by the fact the Fed's rate maintenance regime until 2008 was entirely dependent on adding/draining as necessary to keep the level of excess reserves in the system at zero. Because of this, the fairly straight and steady line of base money reflects it growing in tandem with a steadily expanding supply of deposits that require reserves.

Then after 2008, base money jumps and becomes volatile as a reflection of the change in rate maintenance regime to a floor system making rate maintenance independent of arbitrarily high levels of excess reserves plus the beginning of QE which added arbitrarily high levels of excess reserves.

Looking at the other component, M1 money supply, the investigation can be narrowed further. Because base money levels were essentially pinned to the components of M1 that carry a regulatory reserve requirement, the pre-2008 disturbances must have been produced by changes in the components of M1 that don't carry a regulatory reserve requirement.

So what's in M1? "M1 includes funds that are readily accessible for spending. M1 consists of: (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) traveler's checks of nonbank issuers; (3) demand deposits; and (4) other checkable deposits (OCDs), which consist primarily of negotiable order of withdrawal (NOW) accounts at depository institutions and credit union share draft accounts. Seasonally adjusted M1 is calculated by summing currency, traveler's checks, demand deposits, and OCDs, each seasonally adjusted separately."

Seems (1) and (2) are the possible suspects and (1) is the likely suspect.

The blue trend away from red -- from early 1991 to late 1993

Following through on the theme from my first comment, there were changes in reserve requirements that may play a role in explaining the movement. See page 12 here starting with "Recent Cuts in Reserve Requirements".

Hi, Jazz.

"I still think that if you're going to look at debt/dollar as a negative economic influence, you should back public debt out of the picture."

I just try to see what the graphs show, Jazz. I don't impose preconditions on them.

Your rationale sounds reasonable to me. However, I generally find that I can make gross errors in data selection and still get comparable results in the resulting graphs. I don't *try* to make gross errors, but it's been known to happen.

geerussell,

I am by no means convinced that the money multiplier is "conventionally used" in the manner you describe.

The strength of the criticism of the so-called "conventional use" arises from the fact that the criticism is so obviously correct. To me this suggests it is obvious to everyone... and that suggests that the conventional use must be other than you claim.

"The dismissal is narrow and very specific to that causal story. It's not a blanket objection..."

Yes, but you are a lot more sophisticated and thoughtful than most of the people that I've seen criticize the money multiplier. So maybe I was having a little fun at their expense. Prodding them a bit. They need prodding, not coddling, Gee.

//

FRED Blog recently showed the components of M1 as a percent of M2; I looked at it here.

The graph supports Jim's statement from a while back, that a lot of M2 funds moved into M1 when "other checkable deposits" were offered. The timing of that mid-1990s hump suggests that your "cuts in reserve requirements" helped bring the change about.

Post a Comment