Bank borrowing from the Fed: Nothing ... nothing ... nothing ... and then BANG!

|

| Graph #1 |

|

| Graph #2 |

I thought it was odd that the seemingly irregular pattern suddenly settled down after 1990 and became for the most part quite regular. Calm before the storm, I guess.

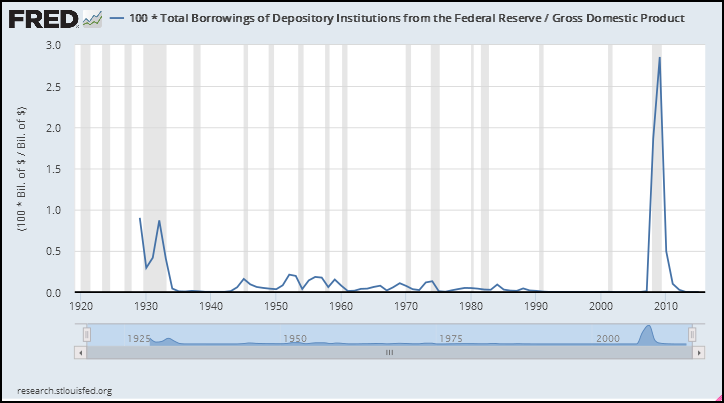

I want to look at the full view again, the one that shows nothing until 2007. But I'll show it "relative to GDP" this time, to give it some context. I'm using the GDPA series (which goes back to 1929) to see far back in time. But it's an annual series. You will notice we lose some of the jiggy detail we had on Graph #2:

|

| Graph #3 |

Let's look at the quiet time.

I want to say banking activity picked up during the second World War, reaching a high point in 1945. But first I want to ask a question: Why do depository institutions borrow from the Federal Reserve?

According to the Board of Governors,

The discount window helps to relieve liquidity strains for individual depository institutions and for the banking system as a whole by providing a source of funding in time of need.Well, they make it sound like the '40s and '50s and '60s and '70s and '80s and '90s all show little crises, small versions of the big bang on the right and the hyperactivity on the left. That was not the case, I'm certain. I'm thinking the banks mostly just needed the money so they could get on with lending.

I could be wrong about that; if I have it wrong, do let me know. In the meanwhile I'm going to say banking activity picked up during World War Two.

The graph shows some pretty good activity in the 1950s. Relatively quiet in the 1960s. More activity in the 1970s again, though less than in the 1950s. Quiet in the 1980s. Then more activity again in the 1990s, but less even than in the 1970s. All calm and quiet after that ... until the crisis.

Here's what I think the graph is telling us: In the period between the second World War and the Financial Crisis of 2007, banks and depository institutions relied less and less on the Federal Reserve as time went by.

Why would this be so? It's not that banks were lending less. No. They were lending more. More and more. But they were relying less and less on the Fed in order to do it.

The graph shows the gradual loss of power of the monetary authority -- the decline in the power of the Federal Reserve.

8 comments:

Art, That looks like a good example of when money is "tight."

It is truly unfortunate that the Fed continues to call that "total borrowings of depository institutions" after the 2008 debacle.

The big spike that started in 9/2008 was loans to bail out the shadow banking system. In other words, that spike was to bailout everybody but the traditional deposit backed banking.

The spike reflects the bailout of the Money Market Funds, commercial paper, and asset backed securities that were the money of account in the shadow banking system. There was a run on the shadow banking system and it took huge sums of money from both the Fed and the US Treasury to contain the run.

Jim: "The spike reflects the bailout of the Money Market Funds, commercial paper, and asset backed securities that were the money of account in the shadow banking system."

Okay, but I want to suggest that "the Money Market Funds, commercial paper, and asset backed securities that were the money of account in the shadow banking system" are an example of banks (including shadow banks) relying less and less on the Fed while lending more and more.

I think my third graph shows the decline of Federal Reserve power over decades due to financial innovation. And I think your remarks offer evidence of it.

Jim,

Are you saying it wasn't a good idea, or is it just a matter of clarification? And with respect to money market accounts, didn't the fed extend FDIC protection to the MM's during the crisis? Art, your point is a good one. (relying less and less on the Fed...) It's also a matter of the removal of barriers on lending by commercial banks with depositors' funds.

Art. if you want to debase the meaning of of the word "bank" to include just about any financial institution go ahead. Everybody else does it nowadays.

Hedge funds can be called banks in the sense that people give them money and they invest it.

But the words "depository institutions" have special meaning in the statutes and before the 2008 debacle the title of the graph was accurate after the 2008 debacle the title on the graph is false. That was the only point I was trying to make.

Nanute, as far as I have seen the FDIC bailed out nobody. They shut down the deposit institutions that had capital shortfalls.

Jim,

The FDIC did, in fact, extend insurance protection to Money Market funds from 2008-2009. There was growing concern that if some funds "broke the buck", it would lead to a run on the funds. That's the only point I was trying to make. While this may not be a technical bail out, it did have the effect of stabilizing these institutions.

I have not seen anything that suggests any involvement of the FDIC.

The US Treasury initially bailed out the MMFs using money from the Exchange Stabilization Fund.

And following that the Fed came up with a whole slew of lending programs that make up that spike in the graph Art posted.

Look up Term Auction Facility (TAF), Term Securities Lending Facility (TSLF), and Primary Dealer Credit Facility(PDCF). All of which allowed financial institutions to put up assets from MMFs and get loans.

Then came Asset-Backed Commercial Paper Money Market Fund Liquidity Facility (AMLF) which was directly targeted at loans to prop up the MMFs.

And then Congress got in on the action with TARP.

Jim,

Seems you are right. My bad. The Treasury program insured the funds on a limited basis. Not the FDIC. https://www.finra.org/investors/alerts/treasurys-guarantee-program-money-market-mutual-funds-what-you-should-know

Post a Comment